While Putin makes loud claims about the Russian economy performing better than those of Western countries, business statistics tell a very different story. Since the beginning of the year, two-thirds of Russia’s largest corporations have either seen a sharp drop in profits or else posted outright losses. The trend is not limited to the hardest-hit sectors, such as oil and gas or coal. Instead, losses and profit declines are being recorded across all industries except banking. A relatively tight monetary policy has brought inflation down, but stock prices are falling again, and the number of defaults is rising. Companies with heavy debt loads and those oriented toward the domestic market are suffering the most. Two major assets have already been nationalized following actions by the Prosecutor General’s Office.

- 1.Sales are there, but profits aren’t

- 2.Only banks are doing well (and far from all of them)

- 3.Construction: debt, nationalization, and transparency issues

- 4.Food industry’s first losses

- 5.Automotive sector: secrets and losses

- 6.Magnitogorsk in the red, Cherepovets with collapsing profits

- 7.Non-ferrous metals: survival depends on size of debt

- 8.Fertilizers are no longer massively profitable

The financial performance of large businesses in today’s Russia says more about the state of the country’s economy than official macroeconomic statistics — in short, the situation in real life looks even worse than the situation on paper. According to the Russian Ministry of Economic Development, GDP was 0.2% lower in January–March 2026 than in the same period last year, yet 0.2% higher in January–April. However, as Vedomosti recently calculated, 21 out of the country’s 28 largest companies saw their situation worsen over the past year, and small and medium-sized businesses fared no better — an increased tax burden resulted in a 22.2% year-on-year decline in tax revenues from SMEs in the first quarter of 2026, the Ministry of Finance admitted.

From Jan. 1 to June 13, the Moscow Exchange index fell by 9%, while the overall decline in the course of 2025 amounted to 4%. The exchange is also recording a sharp spike in bond defaults. While the first half of 2025 saw only 26 defaults involving three issuers, as of mid-June the figure for 2026 had already reached 164 across 16 entities (both figures exclude technical defaults, where companies did ultimately pay their debts after a brief delay).

In the first half of 2026, the Moscow Exchange recorded 164 bond defaults across 16 companies

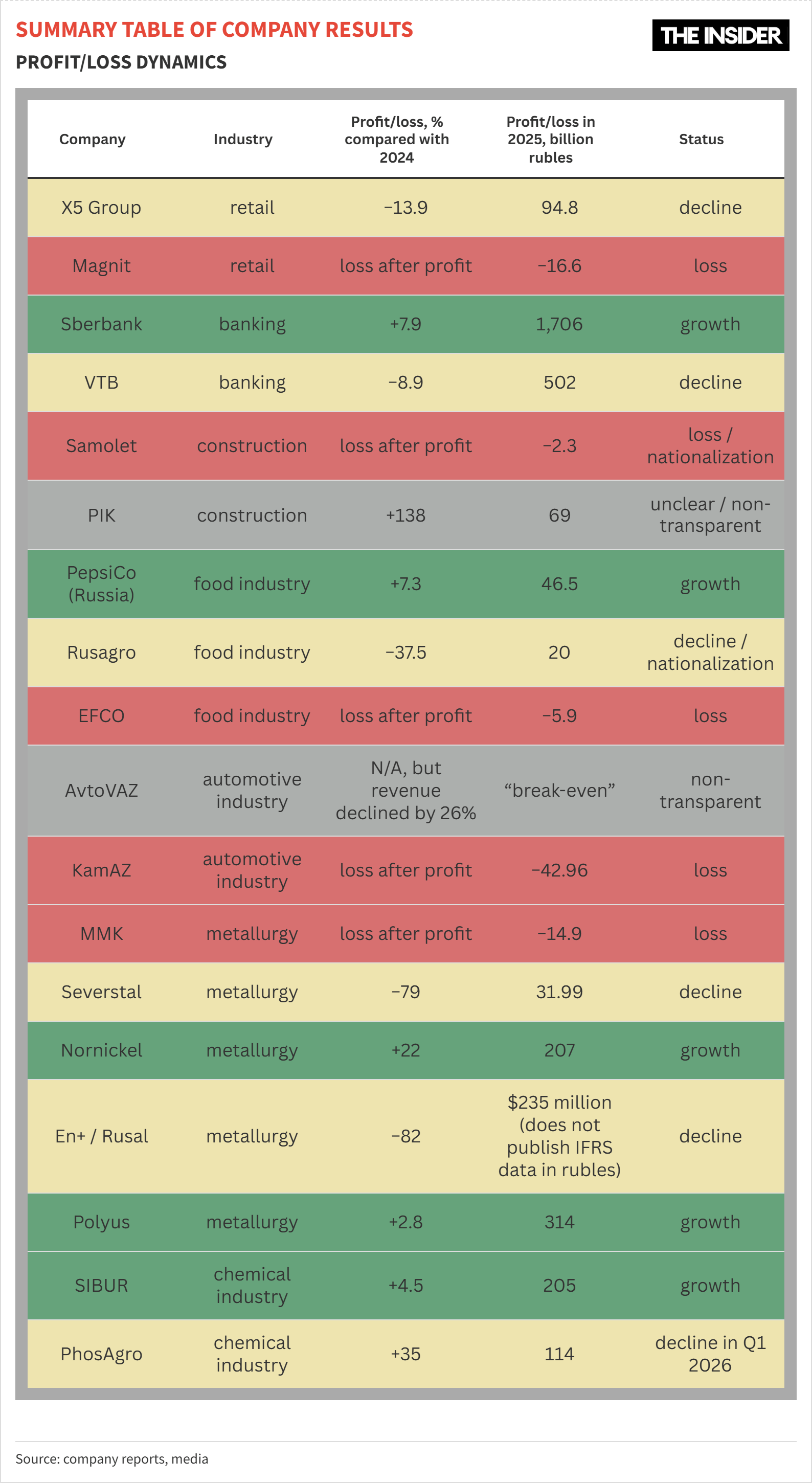

Profit declines and growing losses are observed in almost all sectors except banking. The Insider examined a selection of leading companies in each of the key areas of the economy, excluding state-dominated segments such as the defense and semi-defense industries, infrastructure monopolies, and oil and gas companies. In the services sector, the focus was on retail chains, banks, and construction companies; in the industrial sector, it was on food production, automotive manufacturing, metallurgy, and chemicals.

Sales are there, but profits aren’t

Russia’s largest retail holding company, X5 (Pyaterochka, Perekrestok, and Chizhik food stores), saw revenue grow 19% in 2025, but its net profit fell 14% due to rising costs. X5’s annual report features a dedicated section on macroeconomics and consumer behavior, and it offers some telling assessments.

Amid the optimistic language that echoes Russian government rhetoric, some critical observations slip through: high borrowing costs have reduced business investment capacity; companies were forced to optimize labor costs and cut staffing demand (already felt in late 2025); and high interest rates are prompting consumers to save more and spend less.

The report’s authors note that ”the persistently unstable socioeconomic situation of recent years has triggered a shift in Russians’ consumer habits and strengthened the trend toward rational consumption.” For example, the “downtrading trend” has intensified, with shoppers gravitating away from supermarkets and hypermarkets toward cheaper neighborhood stores and hard discounters.

Economic instability has intensified the “downtrading trend” — a preference for cheaper neighborhood stores and hard discounters

X5’s own hard-discount chain, Chizhik, posted 63% revenue growth for the year, while mid-range Pyaterochka saw growth of just 16%, and the more expensive Perekrestok only 8%. In the first quarter of 2026, the group’s performance deteriorated further: net profit fell 27.6% year-on-year, the number of Perekrestok stores declined for the first time, and foot traffic dropped as well. This means revenue is growing only due to a higher average receipt (the inflation component) and the opening of new stores — primarily of the down-market Chizhik variety.

Russia’s second-largest retail company, Magnit (which owns the Magnit and Dixy chains), has fared even worse. In the spring of 2025, it acquired a controlling stake in the higher-end Azbuka Vkusa grocery chain and carried out a record investment program, expanding its store count by nearly 2,000 in a year — funded by large, expensive loans. Amid weak consumer demand, the move failed to pay off.

True, the group’s operating profit for the year remained substantial at 70.5 billion rubles ($904.4 million), corresponding to a 2% margin (all figures below are presented before the application of IFRS 16). However, its net financial expenses more than tripled — from 24.5 to 82.3 billion rubles ($314.3 million to $1,055.7 million) — wiping out all of that profit. The result was a net loss of 16.6 billion rubles ($213 million), compared to a 50 billion ruble ($641.4 million) profit in 2024. Magnit’s net debt nearly doubled over the year, reaching 496 billion rubles ($6.36 billion), and exceeds 1 trillion rubles ($12.8 billion) when asset revaluation adjustments are taken into account. Magnit’s ambitious gamble has left the company’s future directly dependent on the cost of its debt.

Only banks are doing well (and far from all of them)

Sberbank is among the lucky ones feeling good this year: it grew net profit by 8% in 2025 and reported 17% year-on-year growth in the first quarter of 2026. Both interest income and interest expenses declined, but expenses fell faster, meaning the margin expanded. Asset yield dropped from 17% to 15% over the year, while the cost of funds fell from 13% to 10%.

It turns out that rates for Sberbank depositors are falling faster than for borrowers: Russia’s largest bank continues to take money from individuals and lend it to corporate clients. The public holds 34 trillion rubles ($436.2 billion) at Sberbank, while owing only 20 trillion ($256.6 billion, with two-thirds of that figure coming in the form of mortgage loans). The reverse is true for corporations: their deposits at Sberbank total just 16 trillion rubles ($205.2 billion), while loans extended to businesses have reached 32 trillion rubles ($410.5 billion).

Russia’s second-largest banking group, VTB, has fared worse. While Sberbank’s net interest margin exceeded 6% in the most recent reported quarter, VTB’s reached only 2.5%. The cost-to-income ratio (CIR) is 27% at the more automated Sberbank versus 39% at VTB. Administrative and management expenses remain a serious problem for VTB: they grew 17% over the year, largely canceling out a fourfold increase in net interest income.

The yield on interest-bearing assets fell from 16% to 14.5%, while the cost of interest-bearing liabilities dropped from 16% to 12%. As a result, VTB’s net interest margin, which had been at a critically low 0.7% a year ago, has grown by a factor of more than three. However, the bank cut deposit rates and alienated some depositors. As a result, retail funds at the country’s second-largest bank are shrinking, while they continue to grow at Sberbank.

Construction: debt, nationalization, and transparency issues

While Russia’s largest developer, Samolet Group, posted a net profit of 8 billion rubles ($102.2 million) in 2024, a year later it recorded a 2 billion ruble ($25.6 million) net loss. The causes include the cancellation of mass subsidized mortgages, rising debt servicing costs, and the write-off of investment in the Kvartal Maryino project, which was nationalized in a closed-door court proceeding following a claim from the Prosecutor General’s Office. Adjusted profit (excluding one-time factors) came to 2.5 billion rubles ($31.9 million) — one-third of what it was a year before.

Beyond the nationalization of Kvartal Maryino, Samolet faced other troubles. In March 2025, disgruntled customers stormed one of the company’s Moscow offices in protest over a three-month delay in handing over the keys to apartments they had purchased. In February 2026, the developer appealed to the government for support to ease its financial burden. In early May, the company allowed a technical default on its bonds.

The overall effect was clear. Samolet shares were trading at 400 rubles ($5.11) at the end of May 2026, compared to 1,200 rubles ($15.34) a year earlier and 3,100 rubles ($39.62) the year before that. Over two years, the company has lost approximately 87% of its value.

Samolet Group, one of Russia’s largest developers, appealed to the government for support to reduce its financial burden

Another leader in the construction sector, PIK, has fared better, relatively speaking: shares lost only 50% over the past two years. Although PIK reported massive profit growth in 2025 — to 69 billion rubles ($881.8 million) from 29 billion ($371.3 million) the year before — a closer look at the figures shows that revenue grew just 13% and operating profit by 24%. PIK’s profit growth is explained by a sharp increase in financial (interest) income and a reduction in expenses. In short, abandoned investment in its least profitable projects and redirected funds toward debt repayment and building up liquidity.

PIK’s active construction volume as of June 1 stood at 3.9 million square meters, down from 4.5 million a year earlier — a logical contraction ahead of the looming market downturn.

Meanwhile, PIK has recently been observed taking actions that are hostile to minority investors. The company’s largest shareholder, Sergei Gordeyev, sold his shares to an unknown buyer, the entire board of directors was replaced, no dividends have been paid since 2021, and in 2025 the company officially scrapped its dividend policy. The performance section on the company’s website has not been updated since 2020. This disregard for shareholder interests raises suspicion that PIK’s financial reporting may also be embellished.

Food industry’s first losses

Russia’s largest food and beverage producer is the local PepsiCo subsidiary, which launched its operations back in the 1970s, long before the collapse of the Soviet Union. The company has maintained its position in the Russian market ever since, and revenue continued to grow in 2025 as well. Profit is still increasing, though at a slower pace than before.

In addition, Lay’s snacks, Wimm-Bill-Dann dairy products, and beverages that are now sold under Russian brand names remain in demand. In this sector, abandoning large-scale advertising campaigns has actually had a positive effect on profitability. Russian-origin food companies, however, are faring worse.

The Rusagro Group ranks first in Russia for sunflower oil and mayonnaise production, and second for pork and sugar. In 2025 the company reported an 18% increase in annual revenue, but profit fell from 32 billion rubles ($409.7 million) to 20 billion rubles ($256 million), a decline of 37.5%. The main reason, according to the CEO’s comments, is the rising cost of loans, even subsidized ones.

Meanwhile, Rusagro founder Vadim Moshkovich has been under arrest for more than a year, his shares have been nationalized, and the company has come under state management. For the first quarter 2026, only operational results have been published: revenue grew by just 3%, which is below the inflation rate.

In 2025, the second oil and fat industry giant, Efko (Sloboda and Altero brands), recorded a loss for the first time in its history — approximately 6 billion rubles ($76.8 million), compared with a profit of 7 billion ($89.6 million) the previous year. According to the company’s official statement, the reasons include the high and unpredictable export duty on sunflower oil, the strengthening ruble, logistical constraints on the railway to the Black Sea port of Taman, and expensive loans resulting from the high key interest rate. Efko’s interest expense increased by 14 billion rubles ($179.2 million) — precisely the difference between its 2024 and 2025 financial results. Meanwhile, the company continues to pursue investment projects, including with borrowed funds.

Importantly, Russian vegetable oil producers sell no more than one-third of their output on the domestic market. The rest is exported to countries in Asia and Africa, primarily to India via the Black Sea. As a result, any factor that harms Russian exports — from an expensive ruble and new duties to Ukrainian drone strikes on ports and roads — has a direct effect on the profitability of food companies.

Automotive sector: secrets and losses

Russia’s largest automaker, AvtoVAZ, is a non-public company. It is 100% state-owned and is not required to publish financial results. Management stated only that the 2025 results were break-even, despite Lada sales falling by 26%.

Until recently, the company was not expecting annual net profit until 2028. It was precisely this gloomy forecast that helped secure an extension of tax benefits for the automotive giant from the Samara Region authorities, enabling the company to “reduce excess borrowing and meet its obligations.” AvtoVAZ representatives described the start of 2026 as the worst months for the Russian automotive market in 20 years.

KamAZ’s reports are more informative: revenue fell by just over 3%, while a modest profit (0.7 billion rubles, or $8.9 million, in 2024 under IFRS) turned into a loss of 43 billion rubles ($547.8 million) for 2025. Q1 2026 results are only available under Russian accounting standards (RAS): KamAZ continues to operate at a loss, though this loss (9.2 billion rubles) is 26.3% lower than that of the same period last year. Debts are also rising: accounts payable grew 45.2% over the year and are now comparable to annual revenue, while interest expenses amount to approximately 10 billion rubles ($127.4 million) per quarter. Due to its debt burden, the company has cut its investment program and will have to abandon the development of several business lines.

“We decided that we would continue investing, but we have of course sharply reduced this year’s investment portfolio. That is, we are not starting any new projects and are focused exclusively on the K5 product. And, of course, there is the maintenance of equipment, buildings, and facilities... Overall, we effectively cut the investment budget by a factor of three. We were forced to close part of our R&D work that was aimed at the longer-term future,” explained KamAZ CEO Sergei Kogogin.

“We obviously need to increase our profitability to cope with the debt burden. Think about it: the K5 mainline tractor was sold for 10–11 million rubles [$127,400-140,000] in 2022, and today we sell it for 7.5 million rubles [$95,500]. How can we make money? Costs have risen sharply over this period, but the price has fallen,” the KamAZ chief said.

Magnitogorsk in the red, Cherepovets with collapsing profits

The Magnitogorsk Iron and Steel Works (MMK) group reported that in 2025 pig iron output fell 4%, steel production dropped 9%, and steel product sales in tonnage fell 7%, including a 15% decline in premium products. Revenue contracted by nearly 21%, and instead of the net profit of 80 billion rubles ($1,019 million) recorded in 2024, a net loss of nearly 15 billion rubles ($191 million) was posted. Free cash flow shrank by a factor of five.

According to the company, the poor results were connected to a slowdown in domestic business activity and deteriorating market conditions amid high interest rates and difficult macroeconomic conditions. Steel production was also specifically affected by difficulties in the Turkish economy.

In the first quarter of 2026, MMK’s position continued to worsen: year-on-year pig iron output was 9% higher, but steel production was 5% lower, the tonnage of steel product sales fell 7%, and premium product sales dropped by 10%. Revenue was down by nearly 19%, and the net profit of 3 billion rubles ($38.2 million) recorded in the first quarter of 2025 turned into a net loss of nearly 1.4 billion rubles ($17.8 million).

The company again attributes this to “continued deceleration in Russian business activity” and “negative trends in the Russian steel market.” MMK has chosen a strategy of cutting capital expenditures, paying down debt, and accumulating liquid assets, but whether the state will allow it to continue doing so remains an open question.

MMK has chosen a strategy of cutting capital expenditures, paying down debt, and accumulating liquid assets

Unlike MMK, Severstal managed to end 2025 with a profit — albeit a greatly diminished one. In 2024, the company was 150 billion rubles ($1.9 billion) in the black, while in 2025 that figure fell to 32 billion ($407.7 million). Revenue fell 14%, even as pig iron production grew 12%, steel production rose 4%, and steel product sales increased 4% (when measured in tonnage).

The Cherepovets-based company attributes the deterioration to falling steel prices, which have moved against the broader inflationary trend. Steel demand has contracted “due to the Central Bank’s high key rate and limited availability of market lending in construction and machine-building, as well as the deferral of infrastructure projects to later periods.”

Severstal’s free cash flow turned negative over the year, with the company citing its large-scale investment program as the reason. Also telling is the shift in the sales mix: the share of semi-finished products increased while that of high-value-added products declined.

Similar trends were observed in the first quarter of 2026. Year-on-year revenue was 19% lower, and net profit nearly vanished, amounting to just 57 million rubles ($267 million) versus 21 billion rubles ($725 million) a year earlier. Negative free cash flow increased, reaching minus 40 billion rubles ($508.7 million) for the quarter compared to minus 33 billion rubles ($419.7 million) a year earlier. At the same time, investments from the major program had to be cut by 34% (to 29 billion rubles, or $368.9 million), and cash on hand for January–March 2026 fell from 38 billion to 5 billion rubles ($483.4 million to $63.6 million). The culprits are falling steel product prices, declining demand for large-diameter pipes, and an overall drop in domestic market demand.

Despite these troubles, Severstal’s largest shareholder, Alexei Mordashov, ranks first in Forbes’s 2026 list of Russian billionaires: his wealth grew by $8.1 billion over the year, and his net worth exceeded its pre-war level for the first time, reaching $37 billion compared to $29 billion in 2021.

Non-ferrous metals: survival depends on size of debt

Russian production of nickel, copper, aluminum, and gold is not as dependent on the domestic market as the steel industry is, so downward trends here are less pronounced.

Norilsk Nickel, which exports more than 80% of its output (approximately 50% to China), ended 2025 with roughly the same financial results as it showed in 2024. Net profit rose 22% in ruble terms and 36% in dollar terms, but the primary driver was exchange rate differences.

Norilsk Nickel’s main owner, Vladimir Potanin, ranks second in the Russian Forbes list, right behind Mordashov. His net worth grew by $5.4 billion in 2025, reaching $29.7 billion — surpassing his personal record of $27 billion set in 2021.

The En+ group — which encompasses the aluminum holding company Rusal and the large hydropower plants associated with it — saw its profit shrink from $1.4 billion in 2024 to $235 million in 2025, even as revenue increased by approximately 20%. Profit from core operations fell only 7%, but most of it was consumed by interest payments — an item of expenses that grew by 42%. Operating profit in 2024 still amounted to approximately $1.4 billion, but interest payments absorbed nearly $1.2 billion of that figure. Nevertheless, the net worth of principal shareholder Oleg Deripaska — who ranks 26th in the latest Russian Forbes list — nearly doubled over the year, from $4 billion to $7.6 billion (in 2021 it was $3.8 billion).

Russia’s largest gold mining company, Polyus, earned more profit than Norilsk Nickel and En+ combined. Although gold sales in ounces declined 18% in 2025, dollar revenue rose by 19%, though revenue in rubles grew by only 2.5%.

The cost of producing gold nearly doubled, reaching $739 per ounce, and the company’s average selling price is roughly 25% below the world market price due to forced discounts. However, it still exceeds $3,400 per ounce, ensuring a healthy margin. Profit barely changed, increasing by only 3%.

Polyus is investing actively, particularly in the development of the Sukhoi Log deposit: the total investment in that project alone stood at roughly two-thirds of annual profit, while dividends consumed roughly half of profit, meaning the company’s cash position declined.

Fertilizers are no longer massively profitable

Among Russia’s chemical companies, the largest profits in 2024 were earned by SIBUR (196 billion rubles, or $2.5 billion), MHK EuroChem (111 billion rubles, or $1.4 billion ), and PhosAgro (85 billion rubles, or $1.1 billion).

Overall, fertilizer producers are still the biggest beneficiaries of the war. When Russian natural gas was cut off from world markets, the cost of this key input rose for foreign fertilizer producers, while their Russian counterparts continued to enjoy cheap gas, boosting their competitiveness. Russian fertilizer exports have risen to record levels — and would have risen further still had the state not imposed high duties on them.

As a result, the performance of individual companies looks uneven. SIBUR’s 2025 financial results are paradoxical: revenue fell 10% and net debt rose 21.5%, yet net profit increased by 4.5%. The company itself notes that its results were affected by the strengthening ruble — costs are primarily ruble-denominated, while revenue has an export component. The increase in net profit is entirely attributable to the revaluation of foreign-currency debt obligations due to exchange rate differences.

MHK EuroChem, like SIBUR, is a private company and neglects the timely publication of its financial reports. The largest fertilizer producer has yet to disclose its 2025 figures, but its closest rival by size, PhosAgro, reported that 2025 revenue was up 13% from 2024 and that net profit grew 35%.

Again, however, this relative success in 2025 may simply have come thanks mainly to exchange rate differences. In the first quarter of 2026, year-on-year revenue was 18% lower, while the cost of goods sold was 16% higher. Operating profit contracted by a factor of almost 2.4, and what remained was consumed by interest payments and exchange rate losses. As a result, PhosAgro’s net profit for the quarter was negligible — just 221 million rubles ($2.8 million) compared to nearly 47 billion rubles ($598 million) in the same quarter of the previous year. Consequently, the company cancelled the payment of its final dividends for 2025. From late March to mid-June, its share price fell by approximately 20%.

In general, the Central Bank’s policy of promoting expensive credit is extremely painful for Russia’s large businesses, which are typically heavily indebted. Across eight key sectors — excluding energy, transport, and the defense industry — The Insider examined 18 leading companies that have disclosed data on the dynamics of their financial results. Five of them are currently operating at a loss, and the primary factor in most cases has been high interest payments.

Another seven companies continue to operate profitably but acknowledge declining revenue or net profit, and AvtoVAZ and PIK lack the transparency to render their positive reporting credible. Only four corporate giants continue to grow their profits under the current conditions: Sberbank, Polyus, Norilsk Nickel, and PepsiCo.

Export-oriented enterprises, if they are not overburdened with debt and do not suffer too badly from sanctions, are generally better off than those operating in a shrinking Russian market. The survival formula in conditions bordering on recession is simple: avoid risk, do not count on a demand recovery or cheap credit, urgently cut capital expenditures (or even the overall scale of operations), pay down debt, and stockpile cash. But such actions themselves push the economy toward a more pronounced crisis and are decidedly unwelcome to the government.

A dilemma emerges: either demonstrate solidarity with the state’s official optimism and face the risk of bankruptcy, or show skepticism and risk incurring the wrath of the authorities. Two companies mentioned in this review have already suffered from arbitrary nationalization, meaning the threats that the security-bureaucratic machine poses to business can be as serious as the objective economic factors.