Russia’s budget deficit in January–April nearly doubled when compared with the same period last year, reaching almost 6 trillion rubles, already far exceeding the annual target. The authorities acknowledge this, but have no intention of changing course: interest rates remain high, and these are combining with higher taxes to squeeze businesses. The rise in oil prices to $95 per barrel — a consequence of the closure of the Strait of Hormuz amid the escalation of the conflict in the Persian Gulf — will partially improve the budget arithmetic, but the difference between optimistic and pessimistic oil-price scenarios amounts to only 3 trillion rubles. That is not enough to close the budget hole or halt the decline in a range of civilian production sectors, some of which are down by as much as 10%. Meanwhile, government debt is growing faster than GDP, and Russia is gradually losing what for the past 20 years had been considered its main macroeconomic advantage: the lowest debt burden among major economies.

Economy: from decline to partial recovery

At the beginning of 2026, the Russian economy shifted from slowing growth to outright contraction. In January, GDP fell by 1.8% year-on-year, and by 1.1% in February. Even Vladimir Putin, during meetings on economic issues, consistently spoke of the deterioration of macroeconomic indicators, noting that “for two consecutive months now, economic momentum has unfortunately been declining.”

But in March, the trajectory changed. According to the Ministry of Economic Development, GDP grew by 1.8% year-on-year, thereby recouping almost all of the previous decline. As a result, first-quarter GDP fell by only 0.3%.

The decline is partly explained by a calendar effect: January 2026 had two fewer working days than January 2025, while February had one fewer day. But the reasons go far beyond the calendar. Naturally, the list of causes should begin with massive military spending and, as a consequence, higher taxes — especially VAT, which at the start of the year was expanded to a wider range of payers, with rate hikes for many. Such explanations are conspicuously absent from Putin’s official statements.

If one looks at the data for individual sectors, it becomes clear that most non-military industries remain under pressure. Industrial production is slightly positive, up 0.3%. However, manufacturing output declined by 0.7%, with production of metals, automobiles, construction materials, paper, printed products, and clothing falling by more than 10%. In these sectors, both demand and production capacity are declining as companies suffer from higher taxes, the diversion of resources into the military sphere, internet restrictions, worsening expectations, and the loss of access to foreign technologies.

Companies are suffering from higher taxes, the diversion of resources into the military sphere, internet restrictions, worsening expectations, and the loss of access to foreign technologies

Among the relatively stable indicators are the unemployment rate (which remains low), consumer spending (which is rising in line with inflation), and real incomes (which still outpace inflation).

Forecasts for the year as a whole remain conservative. The September forecast from the Ministry of Economic Development projected GDP growth of 1.3%, but minister Maxim Reshetnikov said that the estimate would be revised downward in May. Meanwhile, the Central Bank insists that the economy will return to growth in the range of 0.5–1.5%.

“In the first quarter, economic activity slowed. This was partly connected to the economy’s adjustment to tax changes. The calendar factor also played a role,” Central Bank chair Elvira Nabiullina said. “In the second quarter, this factor will work in the opposite direction. In May–June of this year, there will be three more working days than a year earlier. All of this means that a more accurate assessment of output trends can only be made on the basis of statistics for the first half of the year.”

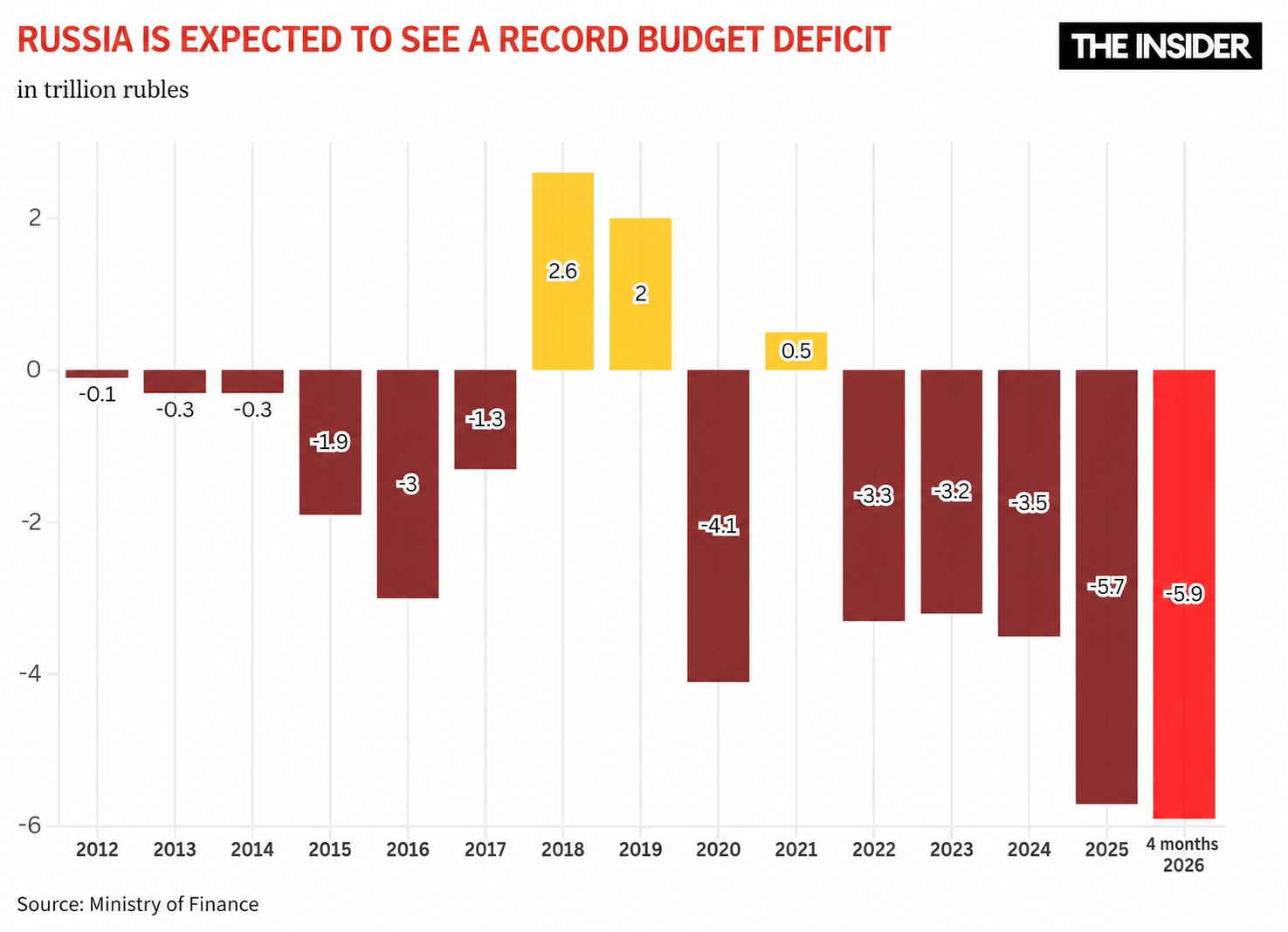

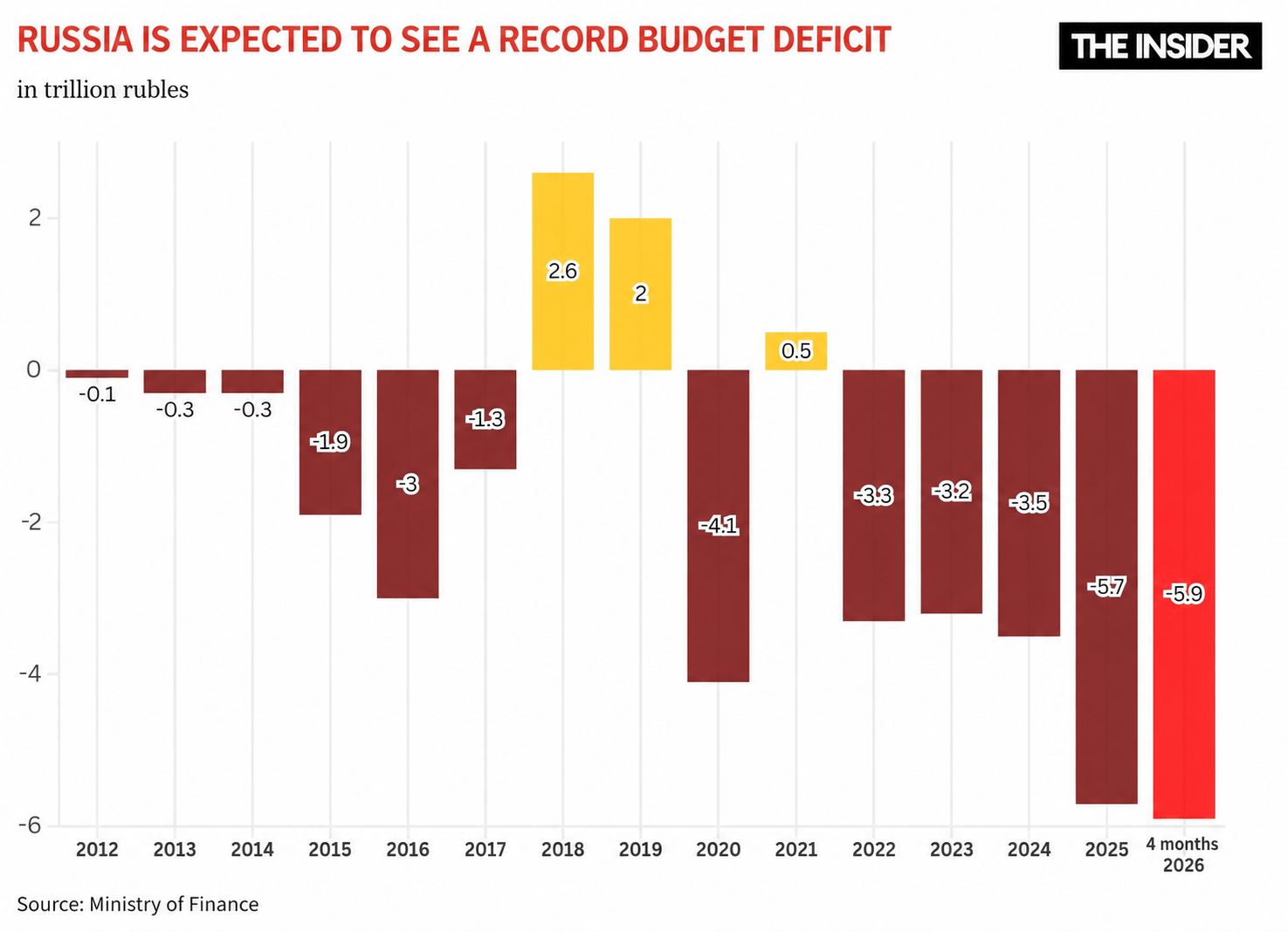

Record budget deficit

The way the state is spending money has also changed. Over the first four months of the year, the federal budget deficit reached 5.9 trillion rubles, already exceeding the planned annual figure of 3.8 trillion. To be fair, the deficit after the first quarter of 2025 was also significant, but at that time the Finance Ministry announced that March had ended with a surplus and that the annual structural balance targets would be maintained. In its commentary on the results of the first quarter of 2026, there is no mention of either point — only a reference to accelerated financing of expenditures.

In January–April, spending rose by 16% year-on-year, and the pattern within the quarter is also notable: in 2026, March spending exceeded February spending for the first time, whereas in 2023–2025 March had been a month of relative budget restraint. In the previous three years, March expenditures amounted to 79–90% of February levels, while in 2026, they reached 110%.

Actual spending in the quarter amounted to 29.2% of the annual plan, although under an even distribution of expenditures it should have been 25%. A direct extrapolation of this proportion to the full year would imply spending of 50 trillion rubles – 13–14% above the planned 44.1 trillion rubles. However, historical data show that overspending at the beginning of the year is generally offset in subsequent quarters: in 2025, the final overshoot amounted to only 3.5%.

If a similar pattern emerges in 2026, annual spending will end up in the range of 45.6–45.8 trillion rubles — still in excess of the planned level, and that’s if, over the remaining nine months, monthly spending does not exceed an average of 3.65 trillion rubles.

The monthly budget balance figures are also telling. Over the past three years, March posted a surplus: revenues in that month are traditionally high because of the schedule for payments of the additional income tax on hydrocarbon extraction, while expenditures are lower. In 2026, however, even March closed with a deficit. Moreover, in 2025 only three months posted surpluses: March, August, and September. The loss of the March surplus this year means that reducing the accumulated deficit in 2026 will be even more difficult.

Russia even ended March with a budget deficit, meaning that reducing the accumulated deficit in 2026 will be even more difficult

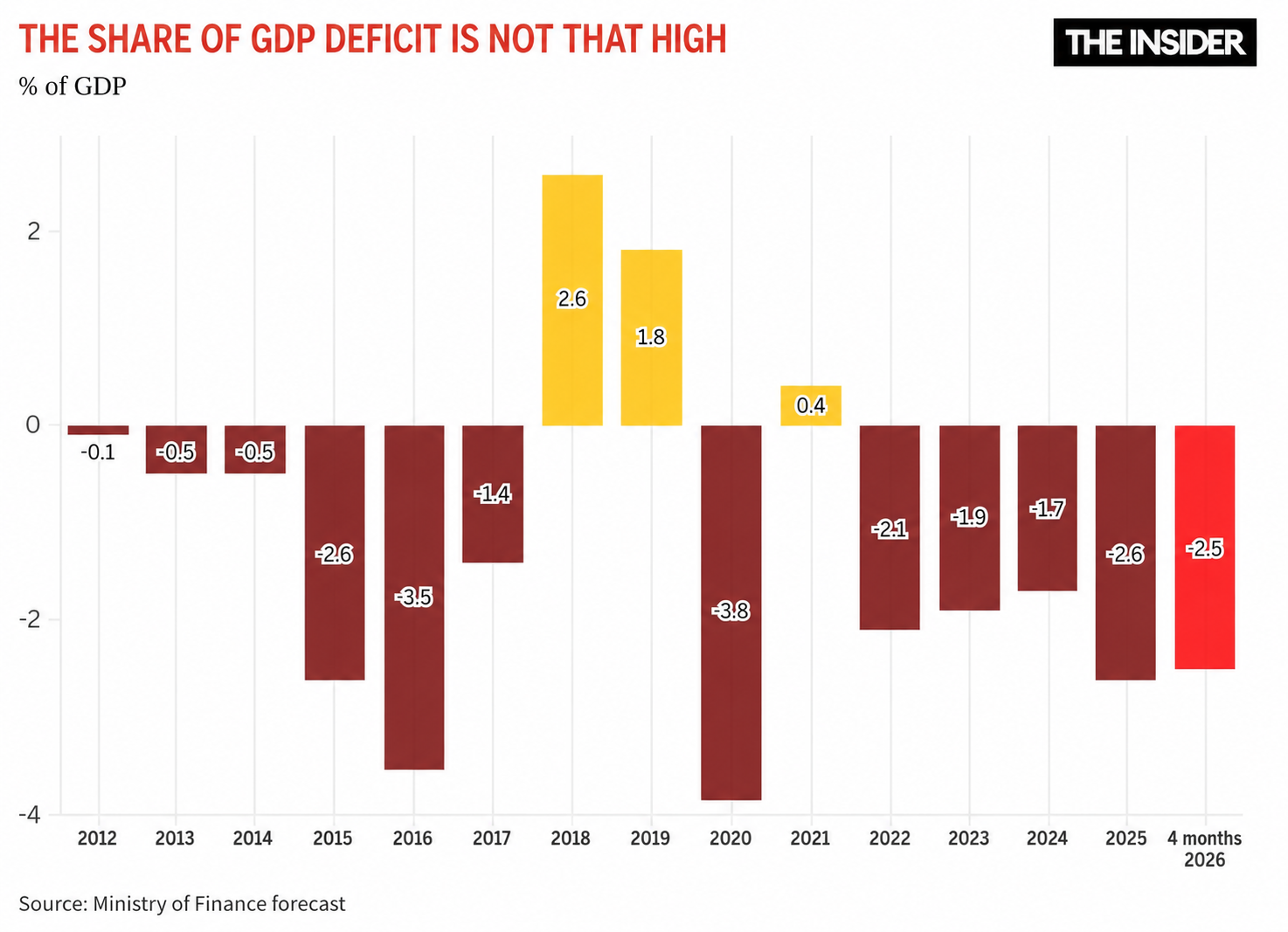

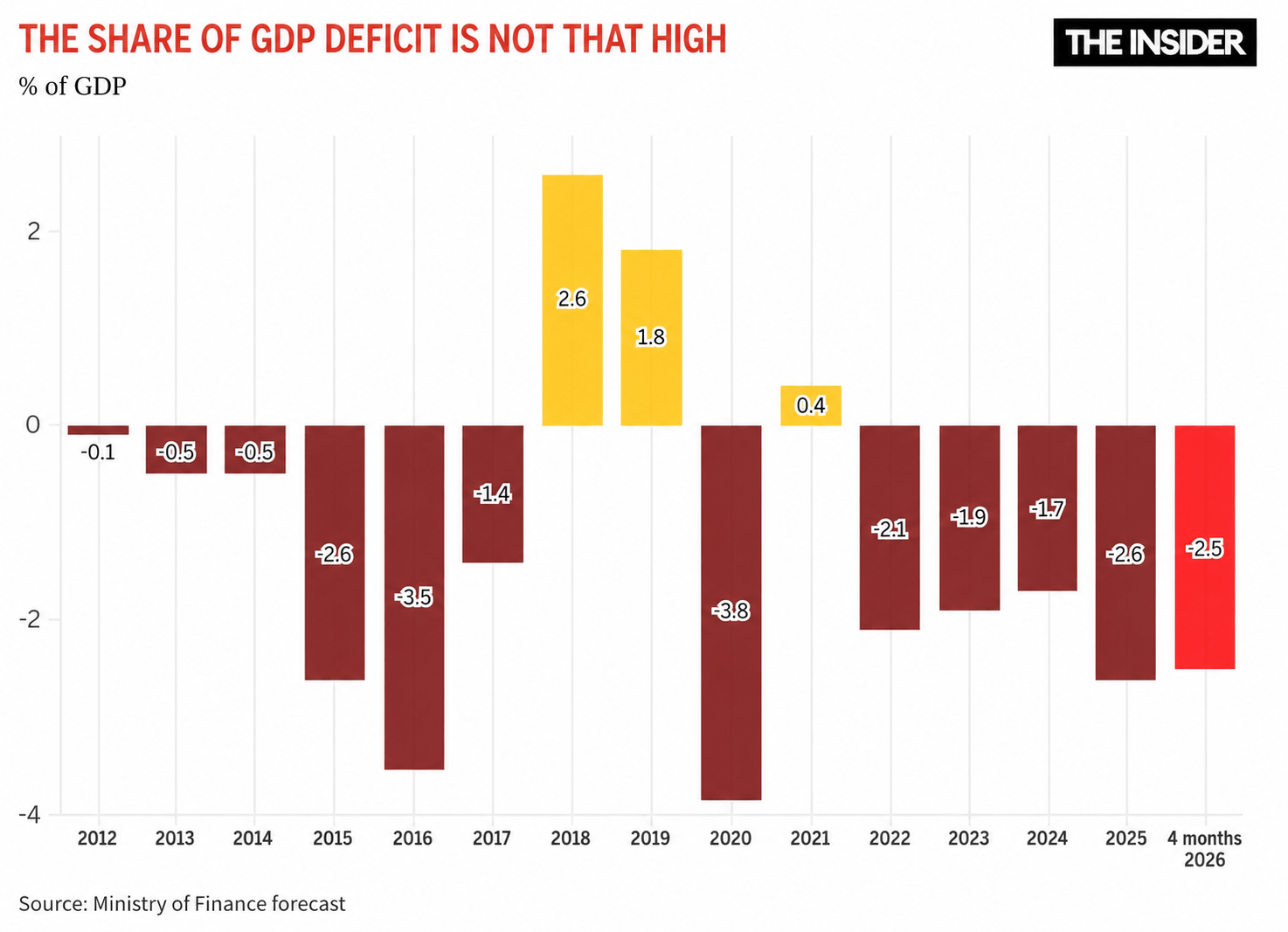

If one assumes that the 8.3 trillion rubles received in the first quarter represent exactly one quarter of total annual revenues, then the full-year figure would amount to 33.2 trillion rubles. And even when using a fairly optimistic estimate of expenditures of 45.7 trillion rubles, this points to a federal deficit of 12.5 trillion ruble, which would be 2.2 times larger than last year’s and nearly 3.3 times larger than the current year’s budget projection. Such a deficit would amount to more than 5% of GDP.

If financed through borrowing, this would mean that domestic government debt would increase by one and a half times over the year – from 30.7 trillion to 43.5 trillion rubles (in 2025 it grew by almost 30%, from 23.7 trillion to 30.7 trillion rubles). And that is only at the federal level, without taking into account regional deficits and debts.

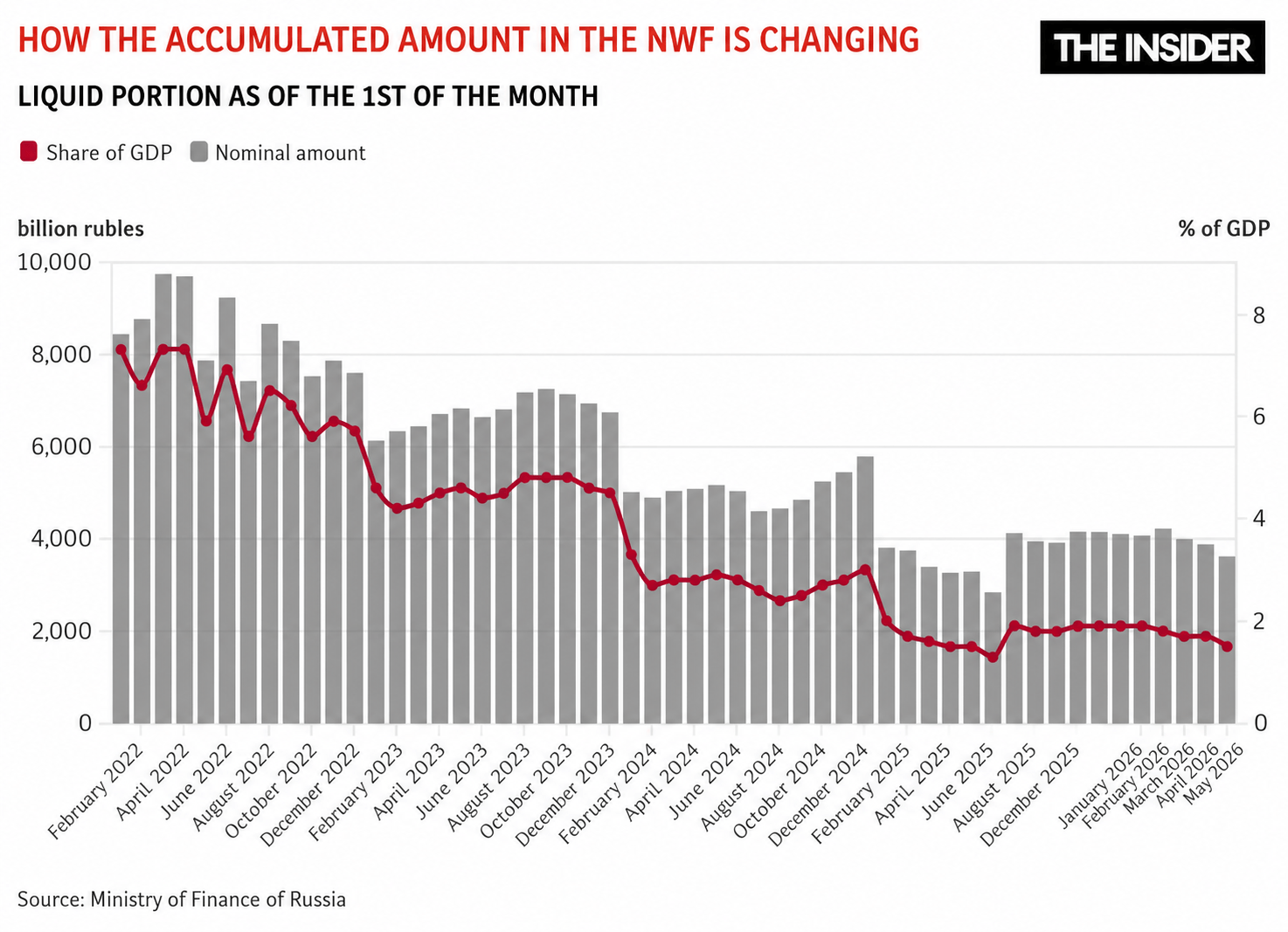

The Finance Ministry has not yet disclosed the sources used to finance the federal deficit in January–March, but they can be inferred from the movement of domestic debt, which rose by 0.8 trillion rubles to 31.5 trillion rubles, and from the liquid assets of the National Wealth Fund, which declined from 4.08 trillion to 3.89 trillion rubles by April 1 and to 3.6 trillion rubles by May 1.

“The deficit shows that the source of financing for expenditures was not taxes, but something else,” says economist and NEST Center expert Sergei Aleksashenko. “In the first quarter, the federal Finance Ministry made very active use of both domestic borrowing and National Wealth Fund money. But most importantly, it sharply reduced the balances in Treasury accounts — a less well-known piggy bank than the National Wealth Fund, but no less substantial. At the beginning of the year, these accounts held more than 9 trillion rubles; by the end of the first quarter, that amount had fallen by 2 trillion. The reduction in account balances is precisely what financed the deficit.”

The government had even prepared to make cuts of 10% to non-priority budget expenditures, but Finance Minister Anton Siluanov later clarified that this was not a cut, but a redistribution. “We never spoke about sequestration at all. The word ‘sequestration’ is the wrong word — we are talking about budget consolidation,” he said in April. “Right now, we are working with the budget through prioritization — increasing funding for the most important items while secondary, less important expenditures are being ‘pushed to the right,’ or perhaps reduced. This is routine work on prioritizing expenditures.”

Aleksashenko explains the shift this way: “Even if a sequestration were carried out, the government could cut roughly one trillion rubles, meaning it still would not cover the deficit. It’s like shearing a pig — lots of squealing, little wool. And it would damage Putin’s image. So according to my sources, when Siluanov came to Putin with the proposal for sequestration, Putin said: ‘Listen, let’s hold off on sequestration for now — things aren’t that bad yet.’”

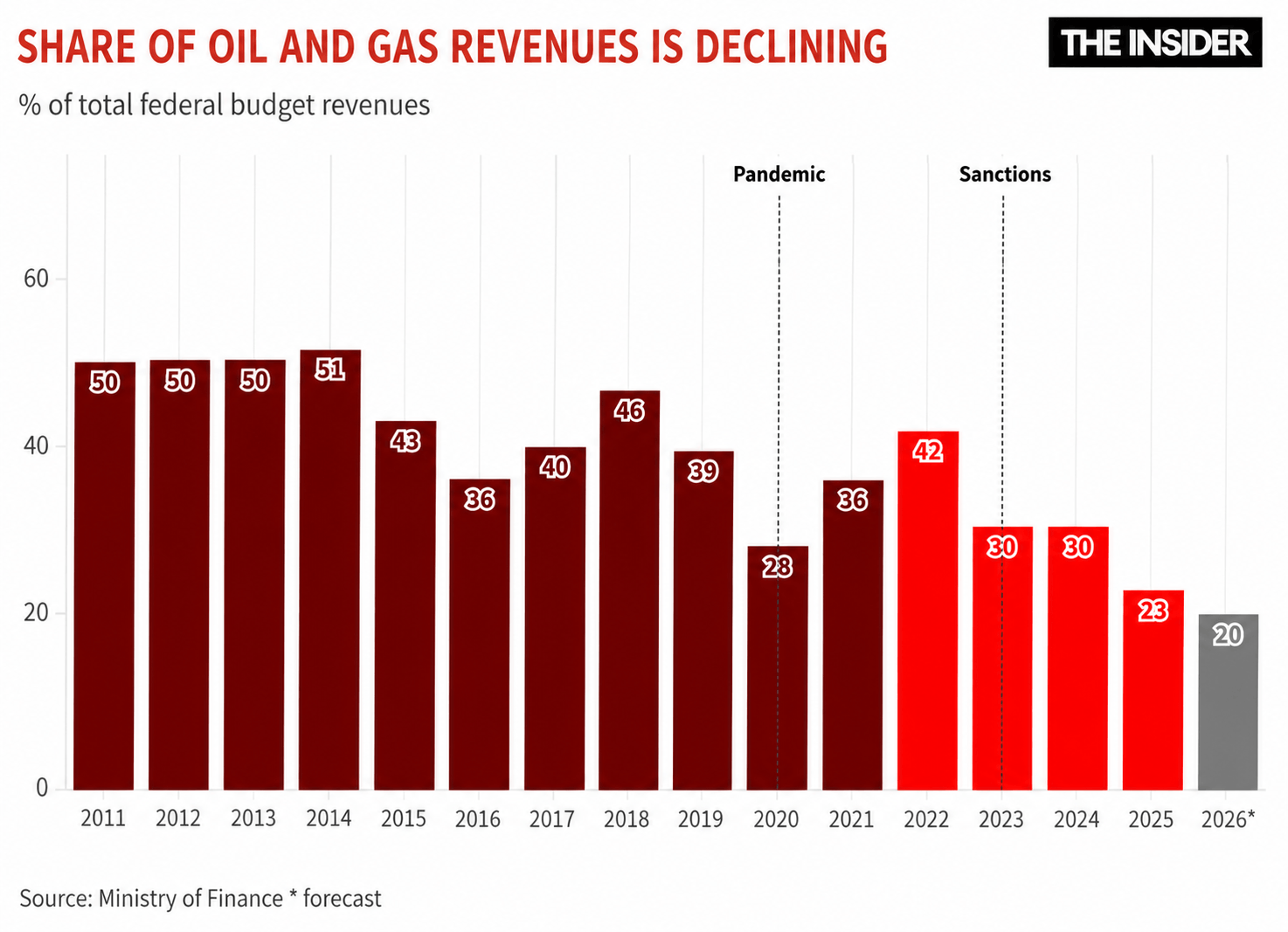

The problem is that oil badly let the budget down at the beginning of the year. Oil-and-gas revenues in January–March were 45.4% lower than a year earlier, although the Finance Ministry can find consolation in the fact that other revenues are growing. “With regard to key non-oil-and-gas revenues, positive growth is being observed both in the federal budget (+7.1% year-on-year) and in the budget system as a whole (+6.7% year-on-year),” officials reported. But what does rising tax collection from the non-commodity sector amid shrinking taxable value added indicate? The answer: an increase in the effective tax burden, which is further slowing the economy.

Expensive oil will not save the economy

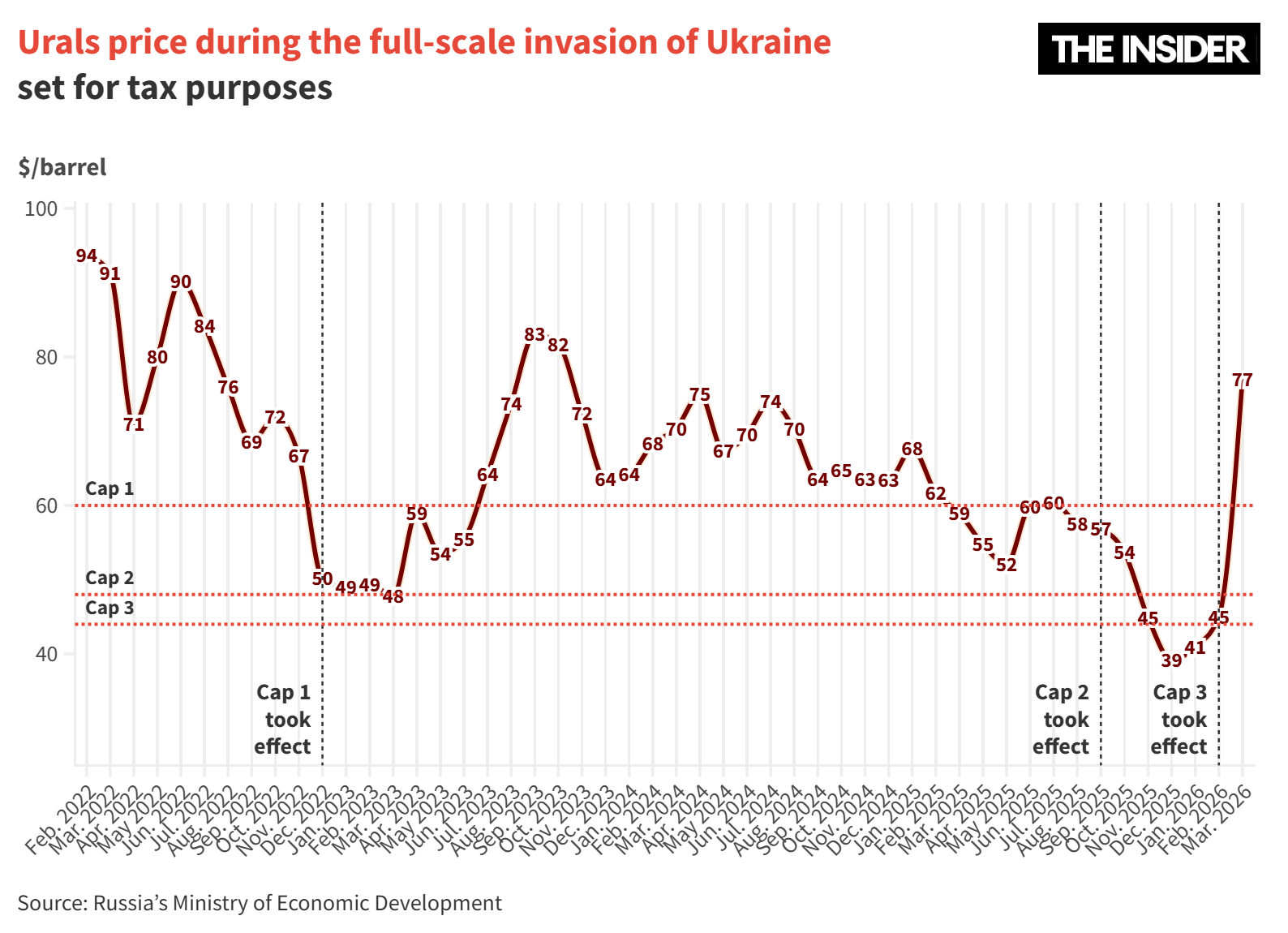

After the escalation in the Persian Gulf, oil prices surged to four-year highs, and in March Russia’s Urals crude actually traded above Brent, a rarity. The average monthly price of Russian oil used by the Ministry of Economic Development for tax calculations rose to $77 per barrel in March, and this was reflected in April budget revenues, which are calculated using March data.

However, oil-and-gas revenues from more expensive oil did not rise as much as expected. In April, oil companies received 207.5 billion rubles in fuel-damper subsidies from the budget. Before that, when prices were very low, they themselves had paid money into the budget under the same mechanism for two consecutive months, albeit in much smaller amounts: 15 billion rubles in March and 19 billion in February.

Revenues in May will be higher, since they are calculated on the basis of April’s price of $94.87 per barrel. For Russia, this obviously means some increase in oil-and-gas revenues. The budget will receive an additional 200 billion rubles because of higher oil prices, Siluanov said. But it is unclear whether he took into account payments to oil companies, or whether they — rather than the budget — will once again receive most of the premium generated by the spike in prices triggered by the conflict with Iran. Even if the entire additional 200 billion rubles goes to the treasury, it would only partially offset the shortfall, which in March amounted to 234.3 billion rubles.

The budget will receive an additional 200 billion rubles in revenue because of higher oil prices

Overall, March could be split into two completely different periods for Russia’s oil sector. Until March 23, export volumes and prices were both rising sharply. Then Ukrainian attacks on the ports of Primorsk and Ust-Luga reduced hydrocarbon shipments, even as prices remained high. As a result, seaborne exports rose by 29% in volume compared with February and by 115% in monetary terms, and it is already clear that April’s high prices will affect budget revenues in May, with the prospect that such market conditions could persist for quite some time.

Even so, this windfall pales in comparison with the “normal” situation in March–April of last year, when at an Urals price of $55–60 per barrel the budget was receiving more than one trillion rubles a month in oil-and-gas revenues. High prices alone are not enough — export volumes also have to be maintained, and here problems have emerged on two levels at once.

First, it is unclear how long the drone-affected ports will remain out of operation, and if successful Ukrainian attacks continue, Russia will be unable to export oil. That would lead to lower production and, consequently, to a reduction in budget revenues, which are calculated on the basis of output.

Second, even oil loaded onto tankers may fail to reach foreign buyers. Ship seizures, physical attacks on vessels, and accidents are becoming increasingly common, all of which raise insurance costs and freight rates.

The optimistic scenario for the Russian treasury would involve receiving just under one trillion rubles in oil-and-gas revenues per month through the end of 2026. In that event, the budget would collect slightly less than 9 trillion rubles over the remainder of the year, even higher than the annual 8.9 trillion rubles projected in the budget (though it still would not reach the record levels of 2022, when oil-and-gas revenues totaled 11.6 trillion rubles).

Under a more pessimistic, albeit rather ordinary scenario, oil-and-gas revenues would remain roughly at March levels: around 600–700 billion rubles per month. That could happen if the Strait of Hormuz is reopened on normal terms. If that happens, full-year oil-and-gas revenues would amount to only around 7.4 trillion rubles.

In any case, the entire difference between the favorable and unfavorable scenarios amounts to about 3 trillion rubles – less than 1.3% of GDP. That is insufficient either to offset the trend toward industrial decline or to fully close the budget “hole.” The share of oil-and-gas revenues in the budget’s income structure fell from 41.6% in 2022 to 17.4% in the first quarter of 2026. This means that rising oil prices alone will not be enough to compensate for the budget’s losses.

Caught in a structural trap

The first quarter exposed a contradiction that cannot be resolved by favorable oil-market conditions. The civilian economy is contracting for deeper reasons: the tax burden is rising, credit is expensive, investment activity is suppressed, and access to technology is limited.

High oil prices may temporarily improve Russia’s budget arithmetic, but they do not change the underlying logic. Even under an optimistic scenario of around one trillion rubles in oil-and-gas revenues per month, the deficit will remain record-high, while expenditures will require either cuts or increased borrowing. Government debt is growing faster than GDP, and Russia is gradually losing what for the past 20 years had been considered its main macroeconomic advantage: the lowest debt burden among major economies.

At the same time, monetary and fiscal policy are both working against growth. The high key interest rate is restraining lending, while higher taxes are eroding business margins. Escaping this combination without structural changes — in the tax system, the allocation of resources between the military and civilian sectors, or in access to foreign markets — will be difficult.

Monetary and fiscal policy are simultaneously working against growth

Nabiullina is right that the calendar factor will work in the opposite direction in the second quarter. But if no recovery follows even with oil at $90 per barrel and three additional working days, that will mean the economy has not merely run into a temporary slowdown, but a structural growth ceiling.

Under the circumstances, the latter would be an entirely natural reality, one far from a worst case scenario. An economic decline of 1–2% a year is actually a fairly mild scenario — wars are usually far more destructive. Annual inflation of 5–6% would seem unusually low for Russia even in peacetime, and after five years of such conditions, Russia’s government debt could reach 60% of GDP and still remain lower than that of each of Ukraine’s key sponsors. In purely financial terms, the country’s margin of stability has not yet been exhausted.

What is absent, however, are any positive prospects for Russia, which will continue to grow poorer slowly and steadily, to fall further behind in development, and to sink deeper into debt once again. The bleakness of this new stagnation will gradually become obvious to everyone. But how that understanding will affect the mood in society and the political situation in Moscow and beyone is not a question for the economists to answer.