The first quarter of 2026 witnessed a sharp decline in investment in Russia, with capital spending down by more than 14% year-on-year. High borrowing costs, higher taxes, and the risk of nationalization are prompting large companies to scale back investment programs, while 80% of small and medium-sized businesses have abandoned any plans for expansion altogether. The suspension of technology and infrastructure projects means the country is effectively living off previously accumulated resources, widening the technological gap between Russia and the outside world. The current investment pause could herald a prolonged structural crisis. Today's cuts in spending on buildings, infrastructure, machinery, and equipment are laying the groundwork for future stagnation. After all, this is how Japan's "lost decade" and Russia's economic collapse of the 1990s began.

Investment in fixed capital in Russia has continued to decline for the fourth consecutive quarter. From January–March 2026, it amounted to 6.6 trillion rubles, down 14% from a year earlier, according to Rosstat. By the end of 2025, overall investment itself had fallen 2.3% when compared with 2024 — the first annual decline since 2020.

Moreover, the quality of investment is deteriorating. Spending on machinery and equipment accounted for 34% of total investment, down from last year, signaling a shift toward less productive forms of capital. Deputy Prime Minister Alexander Novak specified that the bulk of the decline — 307 billion rubles — came from the country's largest companies, including Irkutsk Oil Company, Arctic LNG 2, and Gazprom. Only Rosneft increased its investment, adding 18 billion rubles.

These figures did not trigger panic. On the surface, the rest of the economy does not appear to be doing too badly: the GDP decline seen at the beginning of the year gave way to modest growth (0.3% in January–April); unemployment remained at a record low (2.2% in April); real disposable incomes rose by 1.5% in the first quarter; retail trade turnover increased by 4.3% in January–April; real wages in March were 8.1% higher than a year earlier; and industrial output grew by 1.9% in April.

Yet there are good reasons for serious concern. Investment in fixed capital is one of the key drivers of long-term economic growth. Without it, there can be no expansion of production capacity, no gains in labor productivity, and no technological modernization.

Why investment in fixed capital matters

If companies are not building new facilities and buying new machinery today, there will be no new jobs, no expansion of production, and no gains in competitiveness tomorrow. In this sense, investment is no less important than current GDP growth, the key interest rate, or inflation.

Inflation tells us how much goods and services increased in price yesterday. It is a lagging indicator that merely reflects imbalances that have already emerged. The key interest rate is a policy tool whose effects on the economy are delayed by nine to eighteen months, according to the Bank of Russia. GDP, meanwhile, is the result of past investment — it shows what is happening in the economy right now, but it does not answer the question of what will happen tomorrow.

Investment, by contrast, is tomorrow's GDP. It is a classic leading economic indicator with a long forecasting, meaning it changes before the economy itself does, and its impact can be felt for years to come. While business confidence and PMI (Purchasing Managers' Index) surveys typically anticipate turning points in the business cycle by one to three months and the Composite Leading Indicator (CLI) provides a three- to six-month outlook, investment offers a window three to five years into the future. When a company decides to build a new factory, it is planning for the relatively distant future. That is why falling investment today is a signal that the economy is heading toward stagnation down the line.

Today's decline in investment means economic stagnation five years from now

This warning is already being reinforced by other, shorter-term leading indicators. According to the Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF), Russia’s investment goods supply index in the first quarter of 2026 was 2.7% lower than in the fourth quarter of 2025. The center's analysts noted: "The decline in January, apparently caused by unusually cold and snowy weather in European Russia, was not offset in either February or March."

The current level of investment activity is below not only that of 2024 (by 16%) but also the crisis months of 2022 that followed the start of Russia’s full-scale invasion of Ukraine. By the end of 2025, Russia’s supply of investment goods was down 14% from its level of mid-2024, and it has continued to fall since then.

The Composite Leading Indicator (CLI) for entering a recession reached 0.52 in February — nearly three times the critical threshold of 0.18 and, therefore, a serious warning that economic trouble lies ahead. In March, the latest month for which calculations are available, the indicator declined to 0.46 but remained well above the critical threshold.

On the other side, however, a different indicator suggests that any downturn is unlikely to be prolonged. The Russian construction sector has shown tentative signs of improvement, with CMASF analysts pointing to March as evidence of "a rebound trend." At the same time, they cautioned that "so far this represents only a partial recovery from January's slump; it is clearly premature to conclude that housing demand is rebounding thanks to money flowing out of bank deposits or that conditions in the sector are improving."

All of the leading indicators — construction, the investment goods supply index, the Composite Leading Indicator, PMI surveys, and business sentiment surveys — still suggest that the Russian economy has not bottomed out, and investment, as the leading indicator with the longest forecasting horizon, offers the clearest warning of future stagnation. In three to five years, when existing productive assets wear out and insufficient new capacity has been built to replace them, the economy could enter a tailspin.

What caused the decline in investment?

The slowdown is the result of several factors: expensive borrowing, pervasive uncertainty, cuts in public investment, the high-base effect, and labor shortages.

Factor 1. The cost of money and the lack of affordable credit

Experts at the Pyotr Stolypin Institute for Growth Economics conclude that the private corporate investment cycle has been effectively frozen by the high key interest rate, which suppresses investment through two channels: borrowing costs and deposit yields.

The main obstacle to investment is the high cost of credit. From November 2024 through June 2025, the Bank of Russia kept its key interest rate at 21%, with the average rate for 2025 reaching 19.27%. Although it has since been gradually reduced to 14.25%, borrowing remains prohibitively expensive. The average profitability of Russian businesses is only 10–12%.

In other words, at current interest rates, borrowed funds cost more than the returns generated by most investment projects. Taking out loans to expand production therefore makes little economic sense — virtually all of the potential profit is absorbed by interest payments, leaving businesses with little incentive to commit to long-term investment.

At the same time, high deposit rates also undermine the appeal of investment. Dmitry Belousov, deputy director of the Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF), argues that investment projects become economically viable in Russia when interest rates are at a rate of around 7–8%. "We have created a situation where it is easier and safer to keep money in bank accounts or invest it in OFZ government bonds than to commit it to investment projects whose payback is uncertain," Belousov explains.

High borrowing costs make investment projects unprofitable, leaving businesses with a stronger incentive to keep their money in bank deposits instead

As Alexander Shokhin, head of the Russian Union of Industrialists and Entrepreneurs, observed: "A high interest rate, a strong ruble, high taxes, uncertainty over property rights, and other factors taken together cannot, under current conditions, support business activity or long-term investment."

Back in 2025, Abrau-Durso president Pavel Titov warned that such a monetary policy "does not allow for any meaningful investment." Even retail investors, he argued, prefer bank deposits under these conditions rather than investing in the real economy.

Factor 2. Nationalization, sanctions, and an uneven playing field

Large companies can obtain subsidized loans through government support programs and have access to project financing via VEB.RF and the National Wealth Fund, but small and medium-sized businesses face a fundamentally different reality. According to an Opora Russia survey conducted among 6,600 SMEs, about 80% do not plan to invest in 2026 because they cannot secure financing. As Opora’s president, Alexander Kalinin, stressed: "For many businesses, the question now is not how to grow but how to survive."

Business surveys from the Bank of Russia likewise show that expected demand is only the second most important factor holding back investment — the first is economic uncertainty. According to the central bank's latest Enterprise Monitoring report, investment activity in the first quarter of 2026 fell to average levels last seen at the beginning of 2022, and for the second quarter of 2026, businesses expect the weakest investment growth since the fourth quarter of 2019.

Survey data from manufacturers collected by the Institute of Economic Forecasting of the Russian Academy of Sciences confirm that the problem runs deeper than expensive credit alone. For 40% of respondents, capital investment plans are not determined by interest rates. Instead, the main obstacles are macroeconomic uncertainty and the lack of access to necessary equipment — the latter being a clear result of economic sanctions.

Meanwhile, the term "macroeconomic uncertainty" encompasses more than the risk of further tax increases or cuts in government procurement. It also includes the growing threat of large-scale nationalization.

Factor 3. Labor shortages

Another major factor is the shortage of workers. As noted above, unemployment remains around its historic low of 2.2%, and government officials point to this as one of their main arguments for claiming that the economy is neither in recession nor overheating. However, that does not negate the fact that Russia is experiencing a shortage of skilled workers.

Official estimates put the labor shortage at around 1.5 million people, and some experts believe the true figure is substantially higher. In particular, the Russian Union of Industrialists and Entrepreneurs forecasts that the country's labor shortage will reach 3 million people by the end of the decade.

Factor 4. The high-base effect

The Ministry of Economic Development of the Russian Federation, which describes the 14.3% decline as an expected correction, argues that investment in fixed capital increased by nearly 40% between 2021 and 2024, meaning that the current downturn is, to a large extent, the result of a high comparison base. The ministry also cautions against attaching too much significance to the first quarter, which typically accounts for only about 16% of annual investment. Maxim Oreshkin called the investment figures "very bad" but likewise attributed them in part to the high-base effect.

Maxim Reshetnikov described 2026 as a period of "a pause in investment growth" following the exceptionally high level accumulated in previous years. Experts at the Pyotr Stolypin Institute for Growth Economics concur with the ministry’s conclusions while adding two other important factors: tighter monetary policy and the increase in the value-added tax (VAT) from 20% to 22% on January 1, 2026.

Factor 5. A decline in government investment spending

The government sharply increased the share of public investment during the pandemic, pushing the state's contribution to fixed capital investment to a peak of 20.5% in 2022 (it had been 16.3% in 2019). By the end of 2025, however, this so-called fiscal impulse had fallen to 15.2%. According to the Pyotr Stolypin Institute, the decline reflects shifting government priorities and the reallocation of budget spending.

Meanwhile, the share of investment financed from companies' own funds rose from 53% in 2022 to 63% in 2026, while the share financed through bank loans increased from 10% to 14%. In other words, the businesses that continue to invest are largely those with substantial cash reserves, access to subsidized credit, or sufficient profits to service loans at market interest rates.

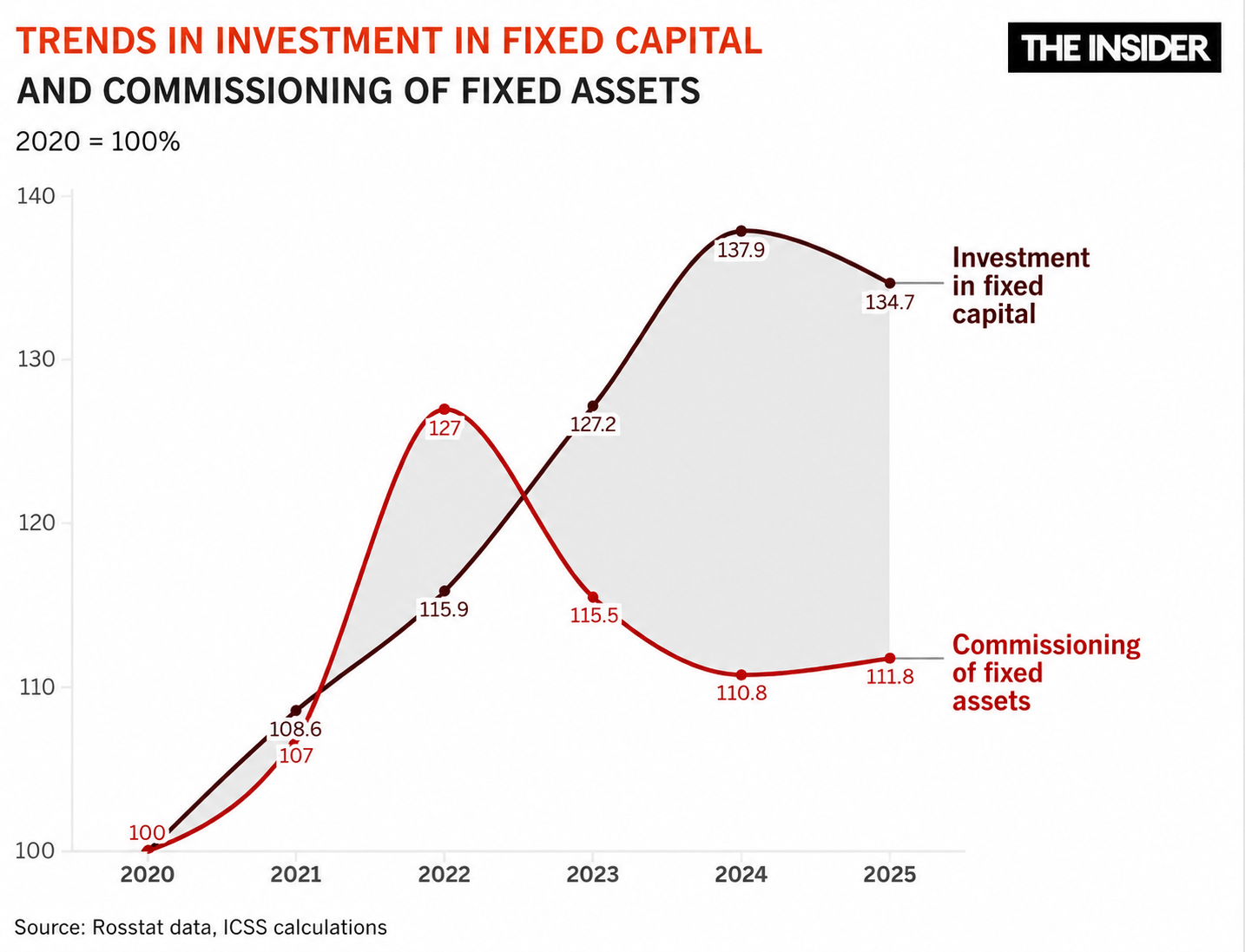

Investment is not only declining; it is also changing — and not for the better. According to the Institute for Complex Strategic Studies (ICSS), the rapid expansion of investment between 2021 and 2024 was not accompanied by a comparable increase in the commissioning of fixed assets — that is, new buildings, structures, and equipment. And indeed, Rosstat data show that the commissioning of fixed assets, measured in constant prices, declined by 9% in 2023 and by a further 4.3% in 2024.

Over the past five years, the commissioning of fixed assets increased by just 11.8%, compared with a 34.7% rise in fixed capital investment — the first time such a wide divergence between the two indicators has ever been observed in Russia.

This points to longer construction timelines, as investment is recorded in official statistics as expenditures are incurred, whereas fixed assets are counted only once projects have been completed and put into operation. It also suggests that investment is shifting away from expanding production capacity toward preserving existing assets. As the Institute for Complex Strategic Studies (ICSS) argues, companies are increasingly reconstructing existing facilities instead of building new ones.

Also, importantly, an increasing number of businesses are investing in measures aimed at "reducing the risk of production capacity being taken out of service," or "ensuring production security." In other words, rather than purchasing new machinery, more and more companies are spending money on air defense systems or drones for the war. As the ICSS report notes, "Part of investment is being directed toward projects that will not result in the creation of new fixed assets (security-related upgrades, dual-use infrastructure, and facilities that fall outside standard statistical accounting)."

Businesses are purchasing air defense systems and drones instead of machine tools – investment is being directed toward security rather than expanding productive capacity

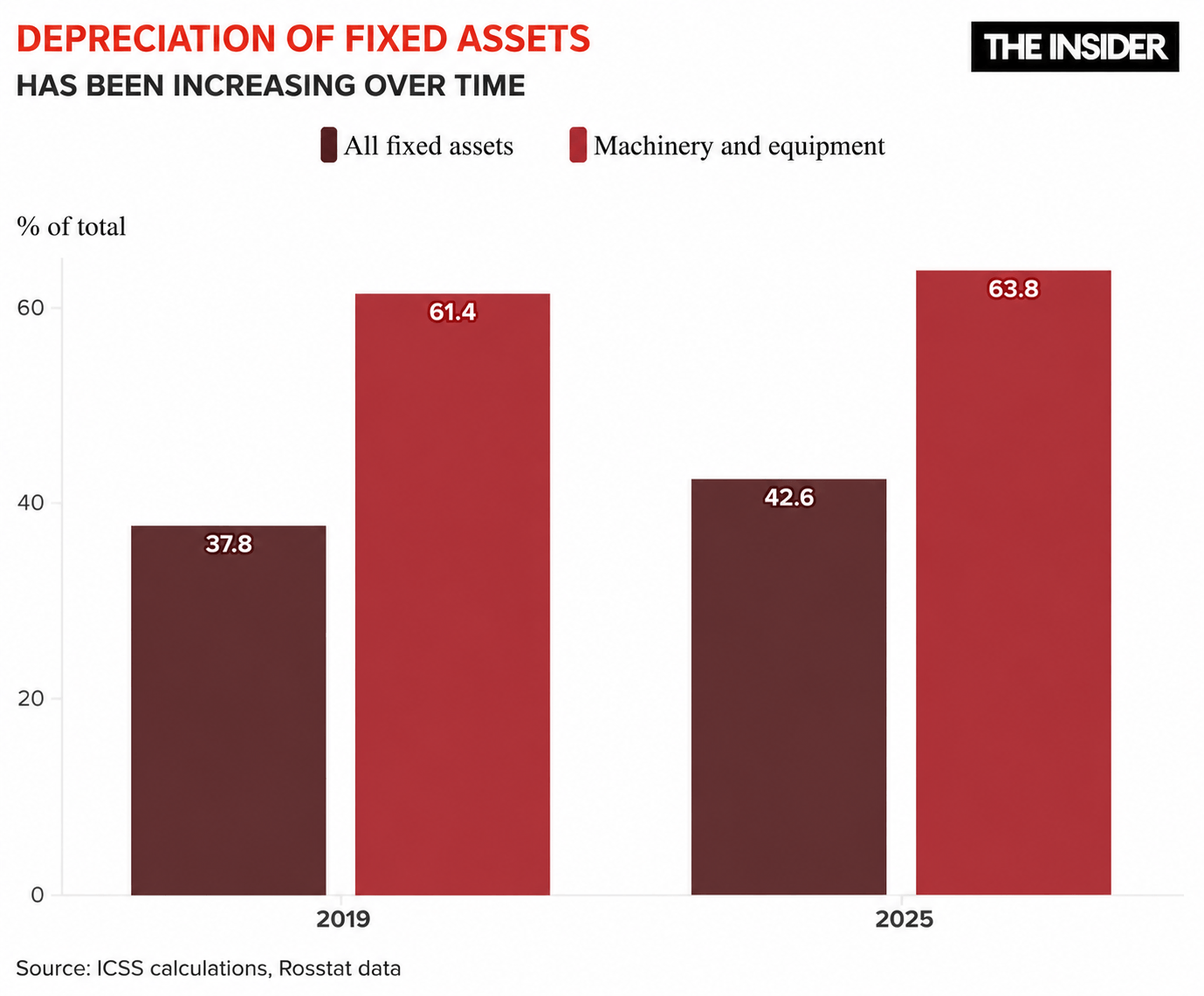

All of this is accelerating the aging of Russia's capital stock. Even before the start of the full-scale war, the country's equipment was already in poor condition. According to Rosstat, fully depreciated fixed assets — those which have been completely written off through depreciation and carry little or no book value — accounted for 22% of the economy's total fixed assets in 2021, the latest year for which Rosstat has published data. In other words, nearly one in every five fixed assets in the Russian economy had reached the end of its service life.

The situation is even worse when it comes to the state of machinery and equipment. The share of fully depreciated machinery increased from 27% in 2017 to 30% in 2020–2021, and between 2017 and 2024, the wear and tear on machinery and equipment increased across most sectors of the economy. In manufacturing, for example, the depreciation rate rose from 57.7% to 63%.

What investment money can no longer buy

While the statistics paint the broader picture, postponed and canceled projects show what those abstract percentages mean in practice. Here are just a few examples of projects that are already running out of investment funding.

Russian Railways: investment program cut for the second consecutive year

The investment program of Russian Railways (RZD) is one of the clearest indicators of infrastructure investment in Russia. It amounted to 1.5 trillion rubles in 2024 but was cut to 891 billion rubles in 2025. In 2026, it was trimmed to 714 billion rubles, and two-thirds of that funding will be spent merely on maintaining existing infrastructure and ensuring transport safety. leaving only 162 billion rubles for the purchase of new rolling stock.

The company hopes to acquire 400 locomotives, but in 2025 it spent 260 billion rubles to purchase the same number. Transmashholding, the manufacturer, has already said that it cannot deliver that order within the proposed budget. "Mathematically, given inflation and rising prices, we as the manufacturer simply do not see how this can work, and we will not fit within that figure," said Georgy Zobov, the company's head of business development.

Russian Railways is facing a severe locomotive shortage, and meeting the targets set out in Russia's transport strategy requires the acquisition of 523 new locomotives each year.

KamAZ: investment budget cut by two-thirds

The retrenchment has also reached the flagships of Russia's automotive industry. According to Sergey Kogogin, the investment budget of KamAZ for 2026 was cut by nearly two-thirds because of rising debt and the continuing crisis in the heavy truck market.

"Just imagine: in 2022, the K5 long-haul tractor unit sold for 10–11 million rubles. Today, we sell it for 7.5 million rubles. How are we supposed to make money? Over that period, our costs have risen sharply, while the price has fallen," the KamAZ chief said.

By the end of the year, KamAZ had posted a record net loss of 43 billion rubles. The cuts affected part of the company's research and development program aimed at long-term projects, leaving funding only for the continued development of the K5 truck line.

Lena River bridge: a symbol of postponed ambitions

Plans to build a bridge across the Lena River near Yakutsk have been under discussion since 1985. Yakutsk is Russia’s only regional administrative center without year-round overland access to the federal highway network. The Lena Bridge was included in the national development program for the Russian Far East as a major capital investment project and was also added to Russia's five-year road construction plan.

Initially, in 2020, the bridge was expected to cost 83 billion rubles. The estimate rose to 176 billion rubles in the fall of 2022 before being revised down to 130 billion rubles, where it has remained despite inflation. Construction began in 2024 but has progressed slowly. According to local media, the bridge is unlikely to be completed until government priorities shift "from defense needs to civilian sectors."

Lithography projects fall victim to budget constraints

At the end of 2025, the Ministry of Industry and Trade of the Russian Federation canceled several tenders related to the development of materials for lithography systems capable of manufacturing chips with process nodes of 90 nanometers and below. These technologies are critical for producing domestically designed processors and other microelectronics.

One of the first projects to be scrapped was a 1.6 billion ruble tender to establish the pilot-scale domestic production of calcium fluoride crystals for optical components capable of being used in ultraviolet photolithography. The ministry also canceled a 400 million ruble project to develop crystals for laser optical isolators.

Another abandoned tender, worth 800 million rubles, was intended to develop a manufacturing process for tantalum capacitor powders, a material used to produce the anodes of oxide-semiconductor and oxide-electrolytic porous tantalum capacitors.

Sources attribute these cancellations to budget shortfalls. Russia's electronic equipment development program faces a funding gap of 33.1 billion rubles for 2026–2028. As CNews reports, funding has been redirected toward projects that the government considers higher priorities.

Investment in agriculture continues to decline

According to the Bank of Russia, investment in fixed capital in the agricultural sector fell by 3.6% year over year in 2025. In March of that year, Russia had about 2,100 investment projects in agriculture and the food industry with a combined value of 4.3 trillion rubles. A year later, that number had dropped to 1,500 projects worth a total of 4.1 trillion rubles. The main reason is the high cost of borrowing, as the terms of subsidized investment loans were tightened in 2025. As a result, Miratorg cut its investment spending in half — to 10 billion rubles in 2025. Its president, Viktor Linnik, explained: "We have not halted a single existing project, but neither have we launched any major new ones."

True, according to Rosstat's preliminary estimates, labor productivity at large and medium-sized companies rose by 1.7% in the first quarter of 2026 after declining by 0.5% over the course of 2025. However, improvement reflects workers putting in more intensive labor — through overtime and heavier workloads — rather than gains driven by technological modernization.

At the same time, in March 2026 real wages surged by 8.1% year-on-year — meaning wages are rising faster than productivity, creating inflationary pressure. Without new investment in equipment and automation, productivity will soon hit its ceiling, leaving the economy with little room for further growth.

Will investment return?

Surveys by the Institute of Economic Forecasting of the Russian Academy of Sciences (INP RAS) show that industrial companies' investment plans remained unchanged from April to May, at minus 13 points. This is an improvement from March but still firmly in pessimistic territory. The Ministry of Economic Development itself has acknowledged that this year's decline will be three times steeper than previously expected: in May, it revised its forecast from –0.5% down to –1.5%. Still, the ministry expects investment growth to resume in 2027, projecting a 2% increase after a two-year pause.

The most pessimistic outlook comes from the ICSS. Its experts conclude that the 2.3% decline in investment recorded in 2025 may mark the beginning of an investment winter in the Russian economy. Moreover, "if current trends persist, the investment downturn in 2026 could prove even more severe" than the Ministry of Economic Development currently forecasts.

The investment pause may signal the beginning of an "investment winter" in the Russian economy

The Russian Union of Industrialists and Entrepreneurs, which represents Russia's largest businesses and whose members account for the bulk of the country's investment, also believes the decline could exceed the official forecast. As Alexander Shokhin noted, "Many sensitive sectors, including digital solutions and robotics, are not merely being put on hold — they are being put into a deep freeze."

What happens if investment does not recover?

If the current investment pause drags on, the economy will begin running down the productive capacity created in earlier years, much of which is already heavily worn out. Without investment in new equipment and the modernization of production lines, these assets will gradually fall into disrepair. As a result, within three to five years the economy could face not merely slower growth but an outright decline in its physical productive capacity.

Another consequence will be a widening technological gap. As ICSS notes, the quality of Russia's fixed assets is also deteriorating, while their technological sophistication has stagnated. The gap separating Russia from the world’s technological leaders — China, the United States, and the countries of the European Union — will therefore continue to widen. At a time when sanctions have made imports of advanced equipment increasingly difficult, this will translate into lower-quality output and reduced production of finished goods.

As history shows, investment pauses tend to become prolonged unless they are accompanied by systemic measures to reduce the cost of capital and establish clear, predictable rules for business. For now, there is little reason to expect such changes in Russia. As a result, the country risks facing either a repeat of the investment collapse of the 1990s.

Lessons from history

Four examples best illustrate the point: there is a direct relationship between capital investment and future growth.

Japan: the "lost decade"

In 1992, Japan's financial bubble burst. The market value of the country's financial assets fell by 1,000 trillion yen, and over the following decade the Nikkei 225 index dropped to a 27-year low.

What was the main cause? Research shows that the answer was stagnating investment, particularly private investment in fixed capital. Japanese companies stopped investing in new equipment, instead paying down debt and repairing their balance sheets — a classic example of what economists call an "uncertainty trap." As a result, Japan's real GDP grew by an average of just 1.14% per year between 1995 and 2002, the weakest performance among the G7 economies.

The "lost decade" eventually became a "lost twenty years," and then a "lost thirty years." When an investment pause drags on for years, a temporary downturn can turn into structural stagnation from which recovery becomes extremely difficult.

South Korea: the "Miracle on the Han River"

In 1960, South Korea was one of the poorest countries in the world, with GDP per capita of only about $79.

After coming to power in 1961, General Park Chung Hee made industrialization and large-scale investment the centerpiece of his economic strategy. Export revenues reached $100 million in November 1964 and $10 billion by 1977. The investment rate increased from 8.6% of GDP in 1960 to 29% in 1988. GDP grew at an average annual rate of 8.4% during the 1960s, 9% in the 1970s, and 9.7% in the 1980s. By 1995, exports had surpassed $100 billion.

By the end of the century, per capita income had reached $33,000. It is a vivid demonstration that capital investment is an investment in the future.

China: investment paid off

China steadily increased capital investment over the course of several decades. Between 1960 and 2011, the share of the country’s GDP dedicated to investment rose from 16% to a historic high of 46%, and despite a relative decline, it remains one of the country's key engines of growth. However, the composition of investment is changing to focus on the spheres of energy, industrial modernization, and high technology.

The Chinese model also has its downsides. Debt levels continue to rise, and generating each additional unit of GDP requires ever greater borrowing. Experts expect the share of investment in China's GDP will continue to gradually decline. Even so, Beijing’s experience demonstrates how sustained capital investment can propel a country to rapid economic development.

Russia: the investment collapse of the 1990s

During the 1990s, investment in fixed capital in Russia fell to what economists described as an "extraordinarily low level," dropping from around 40% in 1990 to just 21% by 1998.

Investment gradually recovered during the 2000s, but companies continued to consume the productive capacity inherited from the Soviet era without creating new capacity to replace it. The country now appears to be on the verge of repeating that experience.