On May 1, the UAE exited OPEC without notifying its partners in advance. The decision was likely driven by two years of accumulated tensions with Saudi Arabia — from the wars in Yemen and Sudan to the personal rivalry between the countries’ rulers, as well as monetary considerations. After investing $150 billion in its domestic production capacity, Abu Dhabi was forced to keep its new infrastructure idle due to its quota, which cost the country tens of billions in lost revenue annually. As long as the Strait of Hormuz remains closed, the market will not feel the change; however, once it opens, an additional one million barrels of Emirati oil per day will effectively function as a direct deduction from the Russian budget, which is already running a deficit three times the yearly target, writes George Voloshin, an expert on international sanctions and CIS countries.

The United Arab Emirates (UAE) withdrew from OPEC and OPEC+ as of May 1. The news was first reported on April 28 by the state news agency WAM. Later, the country’s energy minister, Suhail al-Mazrouei, told Reuters that the decision had been made without prior consultations with cartel partners and described it as political. The official statement from the UAE authorities was succinct: “The time has come to focus our efforts on what our national interest dictates.”

From OPEC to OPEC+: the history of two partnerships

Abu Dhabi joined OPEC in 1967, four years before the emirates achieved statehood. Oil diplomacy preceded sovereignty. The primary goal of the early members was not a quota system, but sovereignty over natural resources: OPEC gave the smaller Gulf states a collective voice against the “Seven Sisters” — the Western majors that controlled production and pricing. The UAE participated in the 1973 oil embargo, which pushed the price of a barrel from $3 to $12 within a few months. In 1971, the Abu Dhabi National Oil Company (ADNOC) was established, and between 1974 and 1976, Western concessions were replaced with equity participation structures featuring a majority state stake.

In the first 40 years of existence, OPEC enjoyed unrestrained growth. UAE production alone increased from 300,000 barrels per day in the first half of the 1970s to 2.5 million barrels by the turn of the century. Membership in the organization provided price stability, international recognition, and access to a major platform for dialogue with consumers.

Created in 1976, the Abu Dhabi Investment Authority (ADIA) is now one of the world’s largest sovereign wealth funds, with assets exceeding $1 trillion, accumulated over decades of steady oil revenues.

The UAE’s relationship with Saudi Arabia has historically been built on close alliance. When the price of Brent sank below $9 per barrel in 1986 due to oversupply, coordination between Riyadh and Abu Dhabi helped the cartel formulate a unified response. During the 2000s supercycle, both states increased production in sync. In 2006–2008, the UAE produced around 2.9 million barrels per day.

The UAE and Saudi Arabia were long-standing allies within OPEC and expanded production in sync during the 2000s

A turning point in the oil cartel’s history was the creation of OPEC+ in December 2016. After Brent once again collapsed below $28 per barrel, OPEC for the first time concluded an agreement with Russia and nine other producers. The total production cut amounted to 1.8 million barrels per day, with the UAE quota set at around 2.87 million barrels per day. For Abu Dhabi, this opened a pragmatic framework for engagement with Moscow: both countries regularly coordinated positions within the Joint Ministerial Monitoring Committee (JMMC). The Saudi Arabia – Russia – UAE trio formed the core of the alliance, while other participants played largely symbolic roles.

A key test for OPEC+ came with the April 2020 deal. When negotiations collapsed in March and Saudi Arabia launched a price war against Russia, the UAE initially backed Riyadh by increasing supply. Oil prices dipped below $20 per barrel, and in April, WTI futures dropped into negative territory for the first time in history.

The price collapse forced the recent partners back to the negotiating table, this time to agree on unprecedented production cuts of nearly 10 million barrels per day across the alliance. Consensus among the three key players was an imperative for overcoming the crisis. The precedent effectively cemented the UAE’s indispensable role in any major oil agreement.

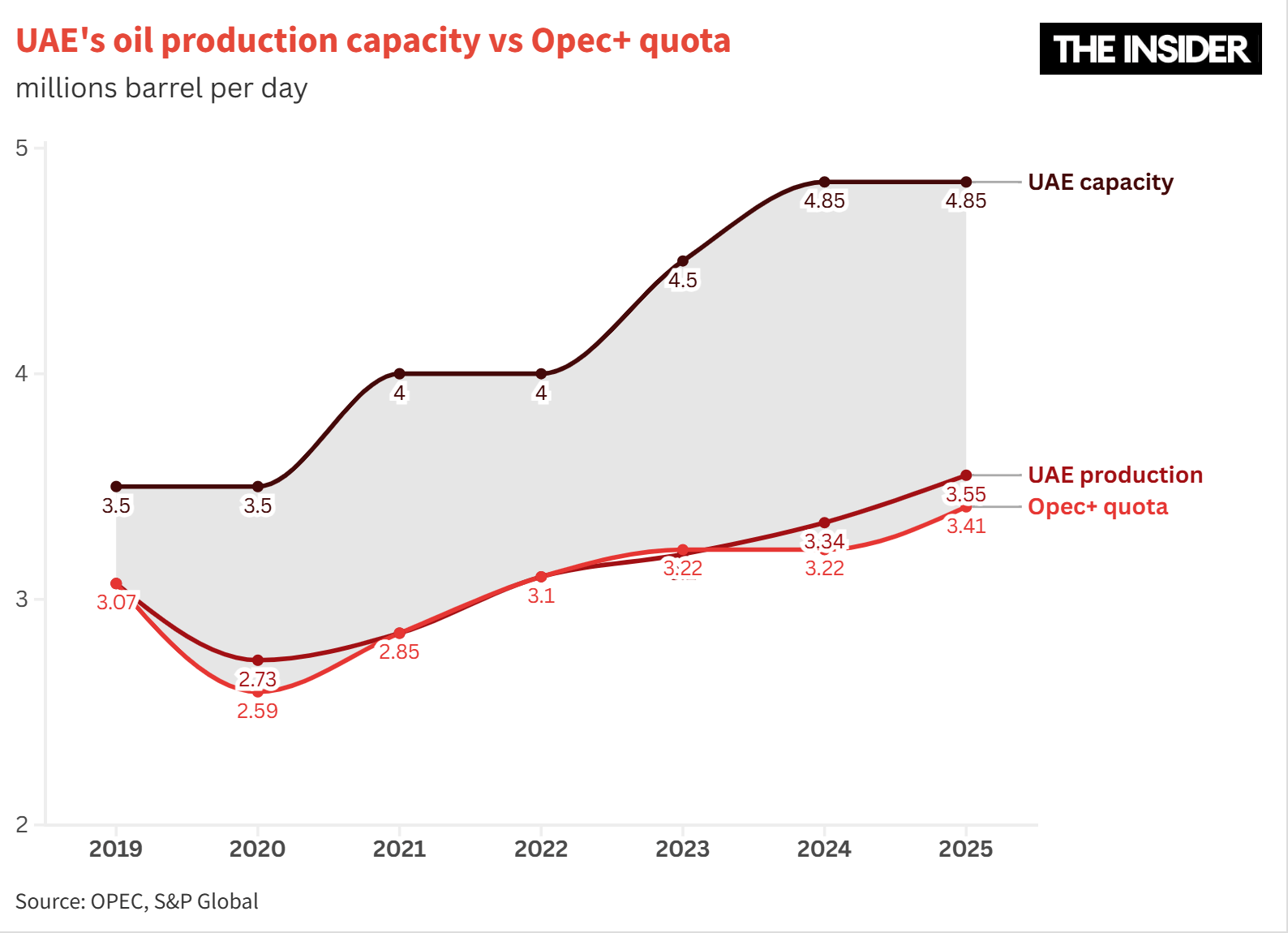

In 2021–2023, ADNOC invested more than $150 billion in production capacity. Output potential soared from 3.5 million to 4.85 million barrels per day, while the daily quota remained stuck at 3.2 million barrels. In June 2023, OPEC+ raised the UAE’s baseline production level to 3.22 million barrels per day, acknowledging the accumulated investments, but this concession only partially eased tensions. By February 2026, the UAE was already producing 3.42 million barrels per day, or 12% of total OPEC output. A situation in which a country that had poured massive funds into infrastructure was forced to keep it underutilized could not continue for long.

The rationale behind Abu Dhabi’s decision

The gap between capacity and quota is not just an accounting issue. At oil prices above $100 per barrel, every 1 million barrels per day of idle capacity translates into more than $36 billion in lost annual revenue. For a country with production costs below $10 per barrel and a fiscal breakeven point of around $50 per barrel — nearly twice as low as Saudi Arabia’s $90 — this effectively amounts to a real tax on its own infrastructure.

ADNOC's 150-billion-dollar investment came with the expectation of reaching full capacity by 2027. On one hand, remaining within the quota system meant effectively financing competitors through its own idle capacity. On the other hand, the International Energy Agency forecasts that global oil demand will peak before 2030. For the UAE, with the world’s sixth-largest oil reserves (113 billion barrels), this is a direct source of concern. Continuing to constrain production within rigid quota limits means leaving money on the table.

However, a purely economic explanation does not fully account for the timing or the tone of the exit. Another factor is a growing political strain that has accumulated over the years. At first, Saudi Crown Prince Mohammed bin Salman and the UAE’s de facto ruler and future president Mohamed bin Zayed, acted in tandem, launching joint military operations in Yemen, the blockade of Qatar, and coordinated opposition to Iran. From 2019 onward, however, their trajectories began to diverge. In December 2025, the UAE-backed Southern Transitional Council seized territories in Yemen that were under the control of Saudi-aligned groups. After Saudi Arabia carried out airstrikes on an Emirati weapons convoy, the UAE withdrew its troops from the country.

The economics alone do not explain either the timing or the tone of the exit; another factor is a growing political strain accumulated over the years

Sudan opened a new front of discord. While Abu Dhabi was arming the Rapid Support Forces, Riyadh backed the regular army fighting them. The two countries found themselves on opposite sides of the world’s largest humanitarian crisis. The UAE’s normalization of relations with Israel under the Abraham Accords — a step Saudi Arabia has yet to take — was perceived in Riyadh as further evidence that Abu Dhabi is steadily moving out of its orbit.

The Iranian crisis became a catalyst for an already emerging rift. Tehran’s missile and drone strikes on Emirati infrastructure unexpectedly called into question the UAE’s membership in OPEC and OPEC+, where Iran is an equally full-fledged participant.

On April 27, UAE presidential adviser Anwar Gargash publicly accused the Gulf Cooperation Council (GCC), which includes both Saudi Arabia and the UAE, as well as Bahrain, Qatar, Kuwait, and Oman, of a “weakest in history” stance. Unlike its GCC partners, which limited themselves to statements of support, Israel provided the Emirates with air defense systems.

Finally, behind all the accumulated contradictions lies the direct rivalry of two OPEC leaders. Over time, the future Saudi king began to view Abu Dhabi as a threat to Saudi hegemony, while the UAE leader, no longer his mentor, turned into an antagonist. Mohammed bin Salman’s Vision 2030 is a direct challenge to the Emirati development model.

Riyadh has long been trying to lure the headquarters of transnational corporations away from Dubai by creating competing projects in tourism and aviation and claiming the role of a regional financial hub. The UAE, which is ahead of Saudi Arabia in economic development by roughly two decades, has no intention of ceding ground. An exit from OPEC/OPEC+ is not only, or even primarily, about oil. It is a symbolic statement of sovereignty.

The end of managed uncertainty: What OPEC stands to lose

As long as the Strait of Hormuz remains closed, the UAE’s exit from both structures will not make much of an impact on the market. According to the International Energy Agency, regional oil production had shrunk by 10 million barrels per day by mid-March. The UAE’s output nearly halved — from 3.47 million barrels per day in February to 1.89 million by the end of March. Meanwhile, oil exports through the strait dropped from 20 million barrels per day to just over 2 million.

Alternative routes — such as the Saudi East-West Pipeline to the port of Yanbu on the Red Sea and the Emirati pipeline to Fujairah — have compensated for only a small portion of the lost volumes. According to Rystad Energy, even under an optimistic scenario, it will take until the end of the year to return to 3.5 million barrels per day. Paradoxically, the very crisis that triggered Abu Dhabi’s demarche is temporarily nullifying its market impact.

OPEC has seen departures before. Indonesia has twice suspended its membership. Ecuador left in 1992 and again in 2020. Gabon exited back in 1995 but returned 21 years later. Qatar withdrew in 2019, officially citing a desire to focus on its core gas sector, though the move also reflected tensions with Riyadh. Angola left in 2024 over a reduced quota. But none of these departures involved the cartel’s third-largest producer, with capacity approaching 5 million barrels per day and accounting for roughly a quarter of OPEC+’s spare capacity. The UAE is a fundamentally different case.

Kazakhstan (a member of OPEC+) and Iraq are being named among the possible candidates to exit next. Kazakhstan has chronically exceeded its quota due to obligations to international oil companies at the Tengiz field. However, the country’s Energy Ministry has stated that it has no plans to change its format of participation in OPEC+.

With the UAE’s departure, Kazakhstan’s influence as a major oil producer within the alliance could even increase. Iraq, the second-largest OPEC producer with a daily output of 4.33 million barrels, has also breached its quotas. However, Baghdad quickly dismissed any speculation, telling Reuters that it has no plans to leave the organization. The remaining OPEC members either fall short of their production quotas or are too dependent on price support to risk an exit.

Saudi Arabia will seek to preserve unity at any cost. At the May OPEC+ meeting, the group agreed on another quota increase — a clear attempt to maintain a sense of normality regardless of the circumstances. The question is not whether Riyadh wants to preserve the alliance, but whether it has enough tools to keep the skeptics on board.

The question is not whether Riyadh wants to preserve the alliance, but whether it has enough tools to keep the skeptics on board

Under the IEA’s baseline scenario, once shipments through the Strait of Hormuz resume by mid-year, supply is expected to recover at a monthly pace of 1–2 million barrels per day. The UAE’s exit is a new factor in this recovery. Abu Dhabi was quick to reassure markets that production increases will be gradual and aligned with market conditions. However, if the UAE ramps up output without quota constraints, Rystad Energy estimates that it could add up to 1 million barrels per day of additional supply over 6–12 months. In a normalization scenario, Brent could move into the $85–100 per barrel range.

If Saudi Arabia responds by increasing production to defend its own market share, and Kazakhstan and Iraq further loosen discipline, the lower bound of that range risks becoming entrenched for an extended period. The UAE’s withdrawal has not dismantled OPEC overnight, but it has forced the organization to give up managed uncertainty for a new setup in which the rules of the game still need to be written.

What should Russia expect?

Moscow reacted to the UAE’s exit from OPEC and OPEC+ in a markedly restrained — and notably swift — manner. Kremlin spokesperson Dmitry Peskov acknowledged that Russia had not been informed in advance, but stressed that Moscow respects Abu Dhabi’s decision. Deputy Prime Minister Alexander Novak also described the UAE’s withdrawal as a “sovereign decision” and ruled out the risk of a price war: “In the current situation, what kind of price war can there be when the market is in deficit?” Russia, Novak added, does not intend to leave OPEC+.

The UAE’s exit from OPEC objectively weakens Saudi Arabia as the cartel’s single dominant leader, while putting Russia in the seat of an indispensable co-chair of OPEC+, now without any potential competition from Abu Dhabi. Notably, throughout 2021–2023, the UAE watched with growing frustration as Russia turned a blind eye to Kazakhstan’s overproduction, while dismissing the UAE’s own claims and grievances.

Moscow views OPEC+ in part as a diplomatic platform that provides regular contact with Riyadh at a time when most channels for international dialogue remain closed for the Kremlin. Relations with the Saudi crown prince, despite periodic tensions, provide a pragmatic working foundation, given the shared interest in keeping oil prices above the fiscal breakeven levels of both countries.

At the same time, since the start of Russia’s full-scale invasion of Ukraine, the UAE has become the largest transport, logistics, and financial hub for the Russian economy. Bilateral trade surged from $5.4 billion in 2021 to $12 billion by the end of 2025. Direct Russian investment in the UAE has exceeded $25 billion.

The UAE has become indispensable for Russia for multiple reasons: from parallel imports of sanctioned goods and components to the transit of gold and diamonds, re-export of petroleum products, and international settlements. Dubai remains one of the few major financial hubs where Russian companies, under sanctions pressure, can still open accounts and conduct payments. Abu Dhabi’s gradual pivot toward the United States, which is interested in weakening OPEC, and toward Israel introduces additional risks for existing channels.

For Russia, any potential concerns still ultimately come down to the state budget. Oil and gas revenues in the first quarter of 2026 fell by 45.4% year-on-year, while the deficit for January–March reached 4.58 trillion rubles, exceeding the planned full-year figure. The Iranian crisis will temporarily reverse the downward trend, and price-cap sanctions will not prevent Russia from securing a war-related price premium.

First, because the price cap is a poorly enforced mechanism that can be bypassed using a “shadow fleet.” (According to the Centre for Research on Energy and Clean Air (CREA), sanctioned tankers already transport about 68% of Russian oil.) Second, the system has become further fragmented once the EU and the UK lowered the cap to $44.1 per barrel, while the United States kept it at $60.

At the same time, structural problems have not gone away: Russia’s Ministry of Economic Development forecasts a budget deficit through 2042. The pain threshold — a sustained price for Urals below $50 per barrel — could again come into play in the event of a global recession or de-escalation in the Middle East.

The pain threshold for Russia’s budget — a Urals price below $50 per barrel — could again come into play in the event of a global recession or de-escalation in the Middle East

Therefore, the prospect of a rapid increase in UAE oil production after the reopening of the Strait of Hormuz is more concerning for Moscow than the UAE’s actual exit from OPEC and OPEC+. An additional 1 million barrels per day of Emirati oil on the market is, in effect, a direct subtraction from Russia’s budget, which is already grasping at straws. The UAE’s new sovereign strategy in the Middle East adds another variable to the geopolitical and geoeconomic equation that will ultimately determine Russia’s ability to finance the war and maintain the current regime.