The price of Urals crude, which surged above $100 after shipping through the Strait of Hormuz was disrupted, fell back to around $50 before rebounding after the re-closure of the waterway. Still, Russia’s federal budget revenues are set to decline by hundreds of billions of rubles. At the same time, Ukrainian strikes on oil refineries are leading to refinery shutdowns that could force producers to reduce oil output. Russia's oil industry not only contributes to the federal budget but also receives subsidies and tax breaks from it, meaning the losses could grow even larger. If oil production declines while budget payouts continue, the budget deficit could multiply several times over. In that event, even the state's financial reserves would not be enough to cover the shortfall.

“I would highlight several key changes in the structure of our economy, including the declining share of the fuel and energy sector, which previously accounted for about 18–20%. Today its share has fallen to 13%, while its share of budget revenues has dropped from 42% to just 22%,” Russia’s Deputy Prime Minister Alexander Novak, who oversees the country’s energy sector, said on July 1.

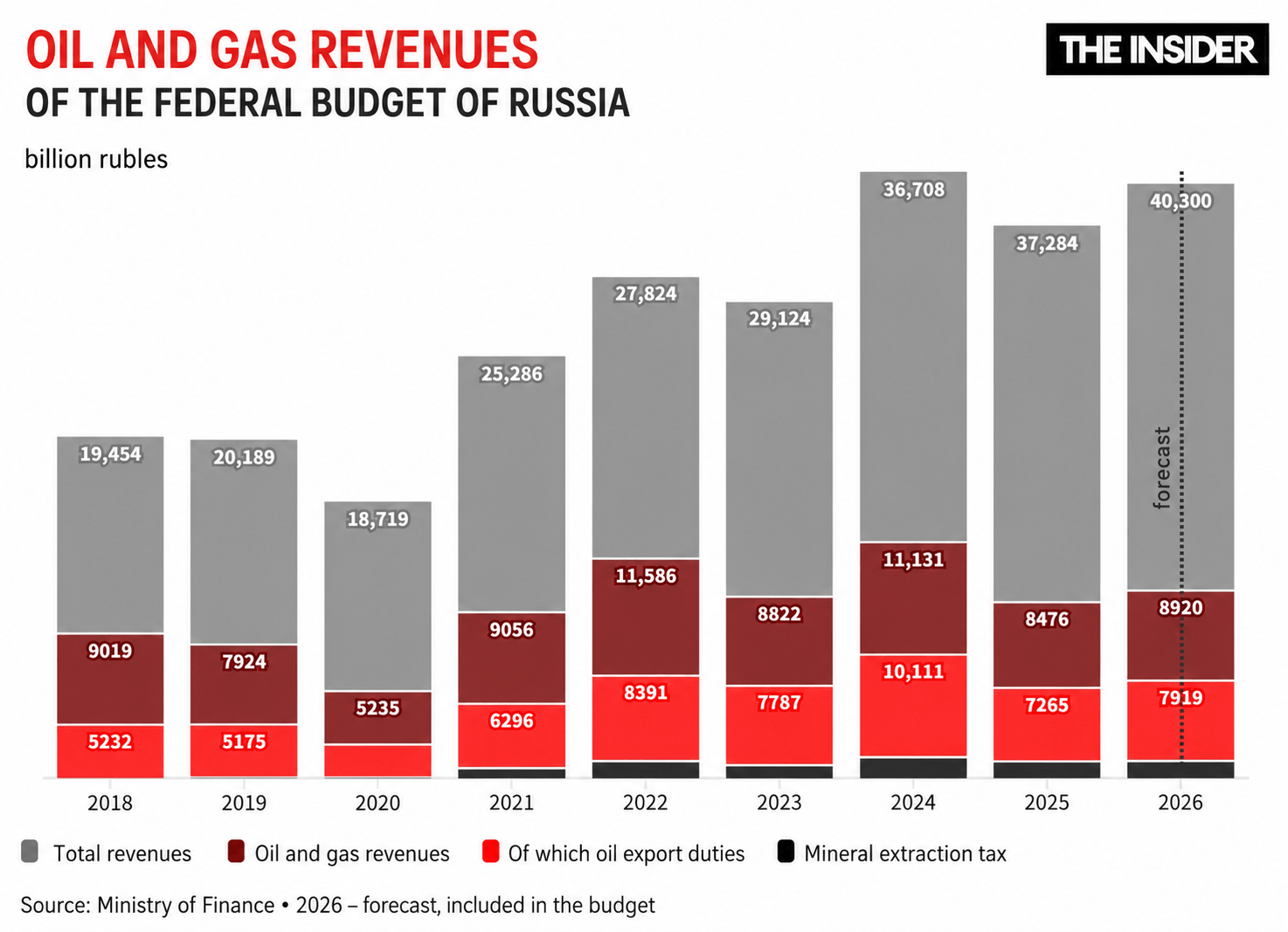

The statistics make it seem as if Russia has weaned itself off its dependence on oil: by the end of 2025, the share of oil and gas revenues in the federal budget had fallen to just under 22% (8.48 trillion rubles, $108.5 billion), and it has continued to decline in 2026. Behind this apparent sign of "recovery," however, lies not the growth of high-tech industries, but rather the effects of sanctions and the peculiarities of a wartime economy.

First, hydrocarbon revenues have fallen — as a direct result of sanctions, and also because of the longer logistics routes that Russian oil must now travel to reach Asian markets (where it sells at a discount). Meanwhile, gas exports to Europe have all but disappeared. In addition, global oil prices hit five-year lows in late 2025 as supply outpaced demand, with production increasing both within OPEC+ and among producers outside the cartel.

Second, non-resource revenues are growing — but not because the economy is expanding. Rather, the government has been forced to raise taxes unrelated to hydrocarbons in order to finance the war. In 2025, after the corporate profit tax rate for most companies was increased from 20% to 25%, federal budget receipts from profit tax rose accordingly. In 2026, this revenue stream is growing further, and the increase in the value-added tax (VAT) — from 20% up to 22% — has also provided a boost to revenues.

As experts at the Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF) described in their January-April review (their last available), the Russian economy is under serious strain:

"Budget system revenues increased by 1.7%. The main factor holding back growth was a 38% decline in oil and gas revenues: higher prices for domestic energy commodities were largely offset by the stronger ruble. Non-oil-and-gas revenues continued to grow (+9%), primarily due to consumption taxes (+18%) and social insurance contributions (+11%). The increase in consumption taxes reflects the higher VAT rate, the expansion of the taxpayer base, and the indexation and rate increases for excise taxes on selected excisable goods.

Growth in taxes on income and profits (+6%) remained more subdued amid weaker corporate profitability. Additional support for budget revenues came from taxes, fees, and payments related to the extraction of non-hydrocarbon natural resources (+22%), including higher mineral extraction tax receipts from gold production amid elevated global gold prices. Customs duty revenues declined (–14%), largely because of the stronger ruble."

As the CMASF explains, budget revenues are rising not because businesses are becoming more profitable, but because the tax burden on them has increased. And the report does not even account for the most recent decline in oil prices.

How money from the oil industry reaches the budget

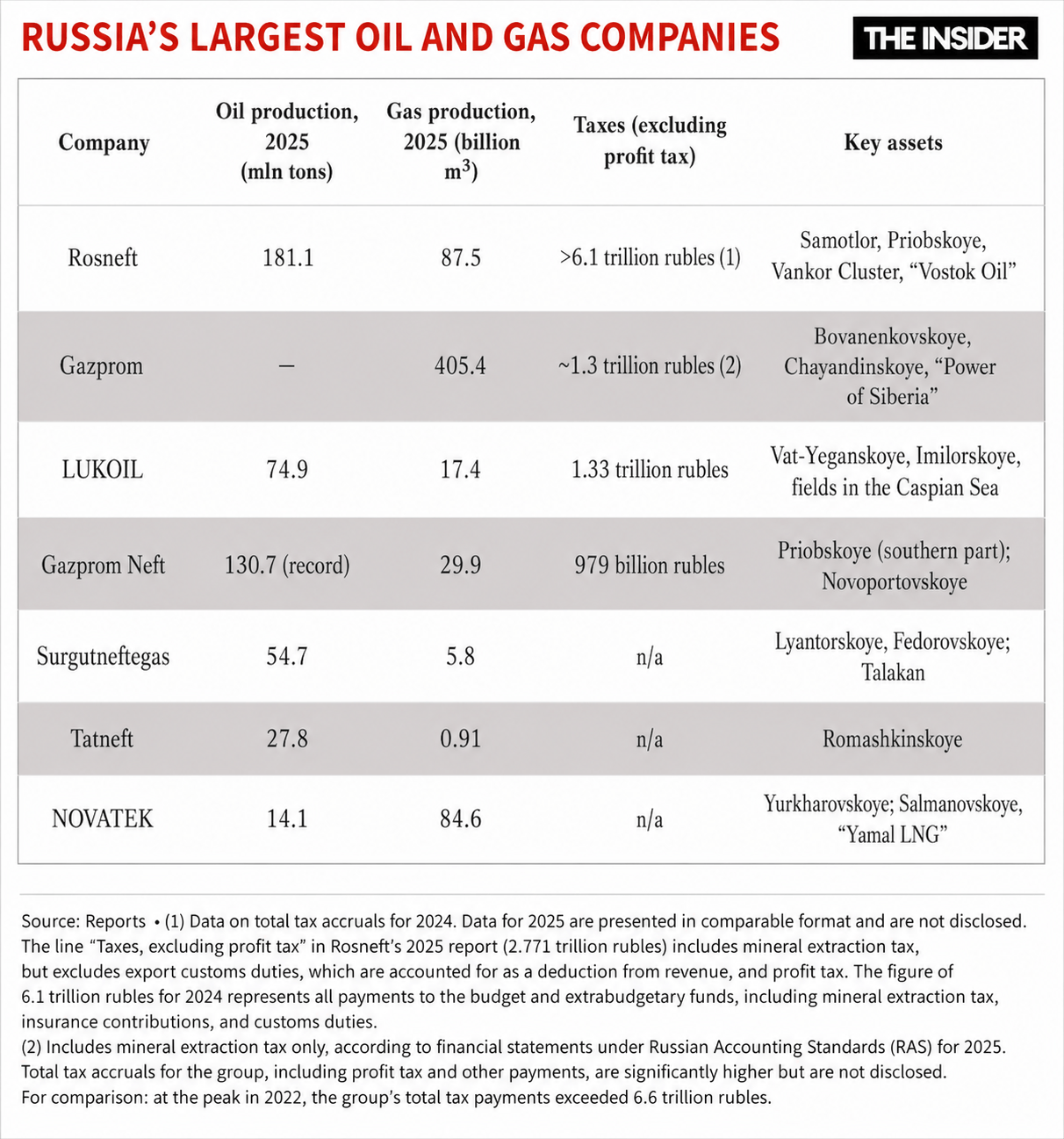

Russia's oil and gas industry is organized as a vertically integrated oligopoly, with the state serving as its largest shareholder and ultimate beneficiary. Two systemically important companies —Rosneft and Gazprom — form the tax backbone of the entire sector.

The industry's tax system has two tiers. First, all companies pay the Mineral Extraction Tax (MET) on everything they produce. This is a direct federal tax, meaning the proceeds go straight to the federal budget. In 2025, total MET receipts fell by 24% (to 8.5 trillion rubles or $108.5 billion), primarily because of the collapse in oil-related MET revenues amid low global oil prices and deeper discounts on Russian crude.

The industry is also subject to the Additional Income Tax (AIT), introduced in 2019. As the name suggests, the AIT applies to the most profitable oil fields. In effect, it replaced the abolished export duty and part of the MET. It is levied on revenue from oil sales after deducting production and transportation costs, making it more sensitive to both oil prices and the ruble's exchange rate. In 2025, AIT revenues amounted to around 1.6 trillion rubles ($20.5 billion), down roughly 20% from 2024.

Since 2022, no public breakdown has been available showing which specific companies and oil fields contribute these revenues to the federal budget. What is known, however, is that Rosneft, traditionally Russia’s largest taxpayer, remains the industry's undisputed leader. CEO Igor Sechin boasted at the company's annual shareholders' meeting that Rosneft paid 5 trillion rubles in taxes and other mandatory payments to government budgets at all levels in 2025. That amounts to roughly 60% of the company's revenue (8.2 trillion rubles or $105 billion), though it was down from the record 6.1 trillion rubles ($78 billion) paid in 2024. The decline mirrored lower oil production: output fell from 184 million metric tons in 2024 to 181.1 million metric tons in 2025. "The change was driven by adjustments to oil production quotas in accordance with government decisions," Rosneft explained.

The company's key assets include the Samotlor and Priobskoye oil fields in Western Siberia, the Vankor cluster in Krasnoyarsk Krai, and the promising Arctic Vostok Oil project, whose resource base is estimated at approximately 6.5–7 billion metric tons of low-sulfur crude.

Rosneft, however, is also first in line when it comes to government subsidies. Since 2017, the Samotlor oil field has received annual tax deductions of 35 billion rubles ($448 million) from the federal budget (when oil prices are high), and beginning in 2024, that amount increased to 50 billion rubles ($640 million). The subsidies are necessary because Russia's largest oil field passed its production peak back in 1980, Sechin explained to Putin, and substantial investment is now required to slow the decline in output. To Rosneft's credit, it has managed to reduce the average annual production decline: between 2008 and 2017, it was 5% annually, but today the figure has fallen to 1%.

The Priobskoye oil field also benefits from tax breaks of a similar magnitude, receiving an annual deduction of 45.96 billion rubles ($590 million). It is a former asset of Mikhail Khodorkovsky’s Yukos, as is its operator, RN-Yuganskneftegaz, which is now Rosneft's main upstream subsidiary. Together, its 40 licensed fields in the Khanty-Mansi Autonomous Okrug account for about 30% of the state-owned company's total oil production.

Lukoil, Russia's largest privately owned oil company, produces a fraction of Rosneft’s domestic output — around 75 million metric tons per year. Its principal asset is the Tevlinsko-Russkinskoye oil field. Excluding corporate profit tax, the company paid 1.33 trillion rubles ($17 billion) in taxes in 2025.

In its annual report for 2025, Gazprom Neft reported a comparable figure: 979 billion rubles ($12.5 billion) in taxes, alongside record production of 130.7 million metric tons of oil equivalent. The company also benefits from temporary tax deductions when oil prices are high: a total of 79.2 billion rubles ($1 billion) from April 1, 2023, through March 31, 2029, with the benefit to be repaid between April 1, 2029, and March 31, 2035. Tatneft and Surgutneftegas are also major taxpayers, although they disclose far fewer production and financial details.

As for natural gas, Gazprom transferred more than 6.6 trillion rubles ($84.4 billion) to budgets at all levels at the peak of the energy crisis in 2022. However, after the Nord Stream pipeline ceased operations, the company became a much smaller contributor to budget revenues. Gas production in 2025 totaled 405 billion cubic meters, down 2.6% from 2024. Its key producing assets are the Bovanenkovo field on the Yamal Peninsula, with initial reserves of approximately 4.9 trillion cubic meters, and the Chayandinskoye field in Yakutia.

Novatek is Russia's largest independent gas producer, with its resource base concentrated on the Yamal and Gydan peninsulas. U.S. sanctions imposed on Arctic LNG 2 in August 2024 effectively froze the country's second-largest liquefied natural gas project. Last year, Novatek produced 84.6 billion cubic meters of natural gas (+0.6% year-on-year) and 14.1 million metric tons of oil (+2.3%).

The group's revenue declined by 6.5% — to 1.45 trillion rubles ($18.6 billion) — primarily because of the stronger ruble and lower oil prices. Net profit fell 63% — to 183 billion rubles ($2.3 billion), weighed down by the higher corporate profit tax rate for LNG producers (34% in 2024-2025, reduced to 25% beginning in 2026). The company does not disclose separate figures for its Mineral Extraction Tax (MET) payments.

Oil refining under attack (in every sense)

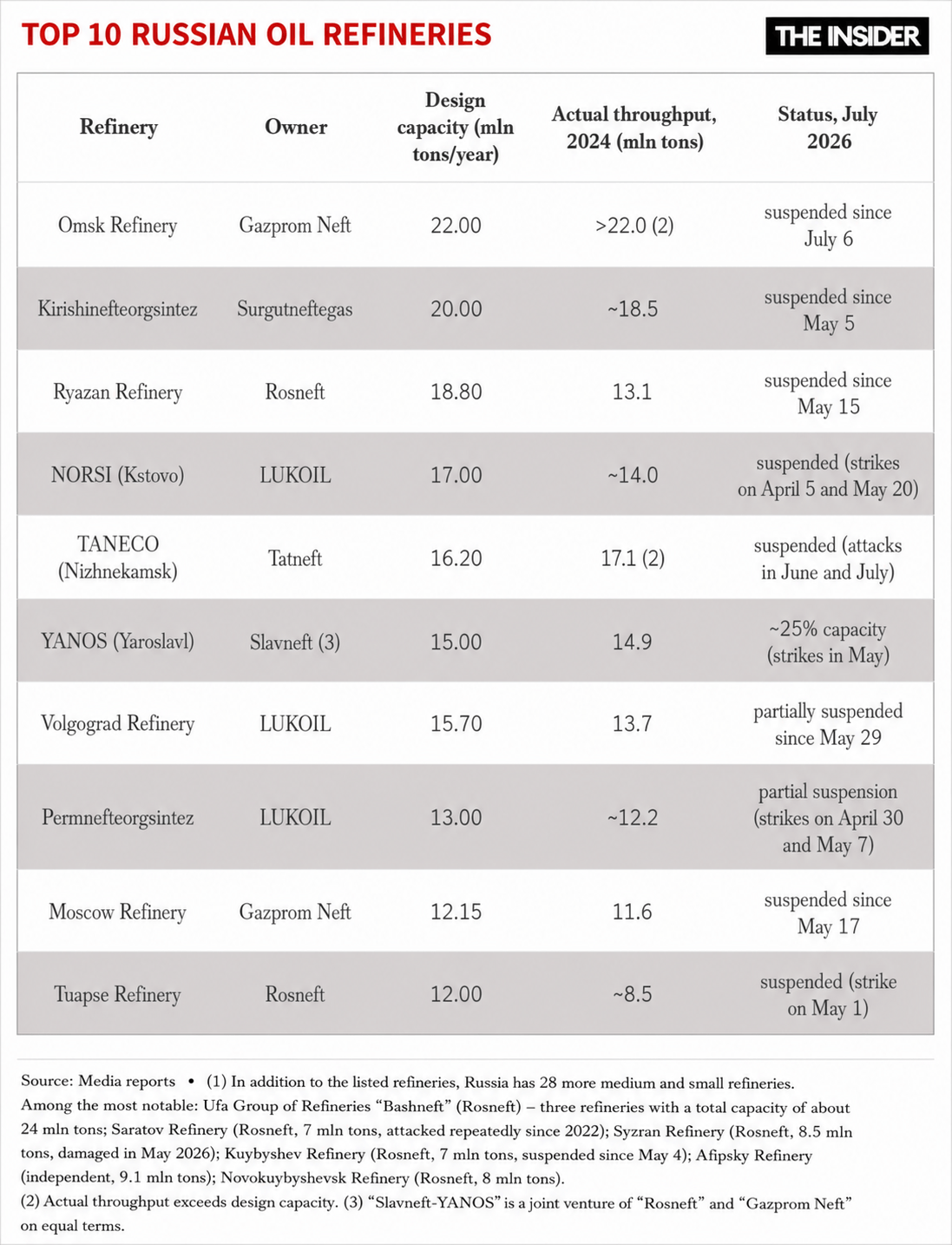

Russia has 38 medium- and large-scale oil refineries with a combined processing capacity of about 330 million metric tons per year. In 2024, they processed approximately 267 million metric tons of crude, the lowest figure since 2012. The financial results of individual refineries are no longer made public — instead, since 2022, all significant figures have been consolidated at the level of their parent holding companies. As a result, the direct revenue losses caused by shutdowns at specific refineries can be estimated only indirectly, by examining the declining performance of the parent groups and exchange-traded indicators for Russia's domestic petroleum products market.

The main structural weakness exposed by the drone strikes is that Russia spent decades concentrating its refining capacity in Central Russia and the Volga region — precisely the areas most heavily targeted in recent months by Ukrainian long-range drones with a range of up to 2,000 kilometers.

Refining capacity has long been concentrated in Central Russia and the Volga region — the very areas where Ukrainian drones operate most intensively

For the first few years of the full-scale war, the Omsk Oil Refinery and the refineries of Eastern Siberia effectively served as a strategic reserve thanks to the fact that they lay beyond the reliable strike range of Ukrainian drones. However, on July 6, the Omsk Oil Refinery was struck, and as the range of Kyiv’s drones continues to increase, the effective strike radius continues to expand.

The industry's direct losses in 2025 alone were estimated at more than 100 billion rubles ($1.3 billion), and when estimates of lost revenue are included, the figure exceeds 1 trillion rubles ($13 billion). For the federal budget, the key issue is that insufficient refining capacity forces companies to cut oil production, largely because of infrastructure bottlenecks that limit the transportation and export loading of crude oil.

In practice, there are three major constraints. The first is the capacity of Transneft's pipeline network. It was designed to handle a certain volume of crude, and there is no spare capacity to rapidly increase exports. The second is port congestion. Baltic and Black Sea export terminals are already operating at or near full capacity, and some have sustained damage. The third is the sanctions imposed in October 2025 against Rosneft and Lukoil, which formally affect about 70% of Russia's export volumes, further narrowing the pool of buyers and available tankers.

Taken together, these factors mean it is physically impossible to increase crude exports quickly enough to offset the loss of refining capacity. Any decline in oil production, in turn, translates directly into lower Mineral Extraction Tax (MET) revenues.

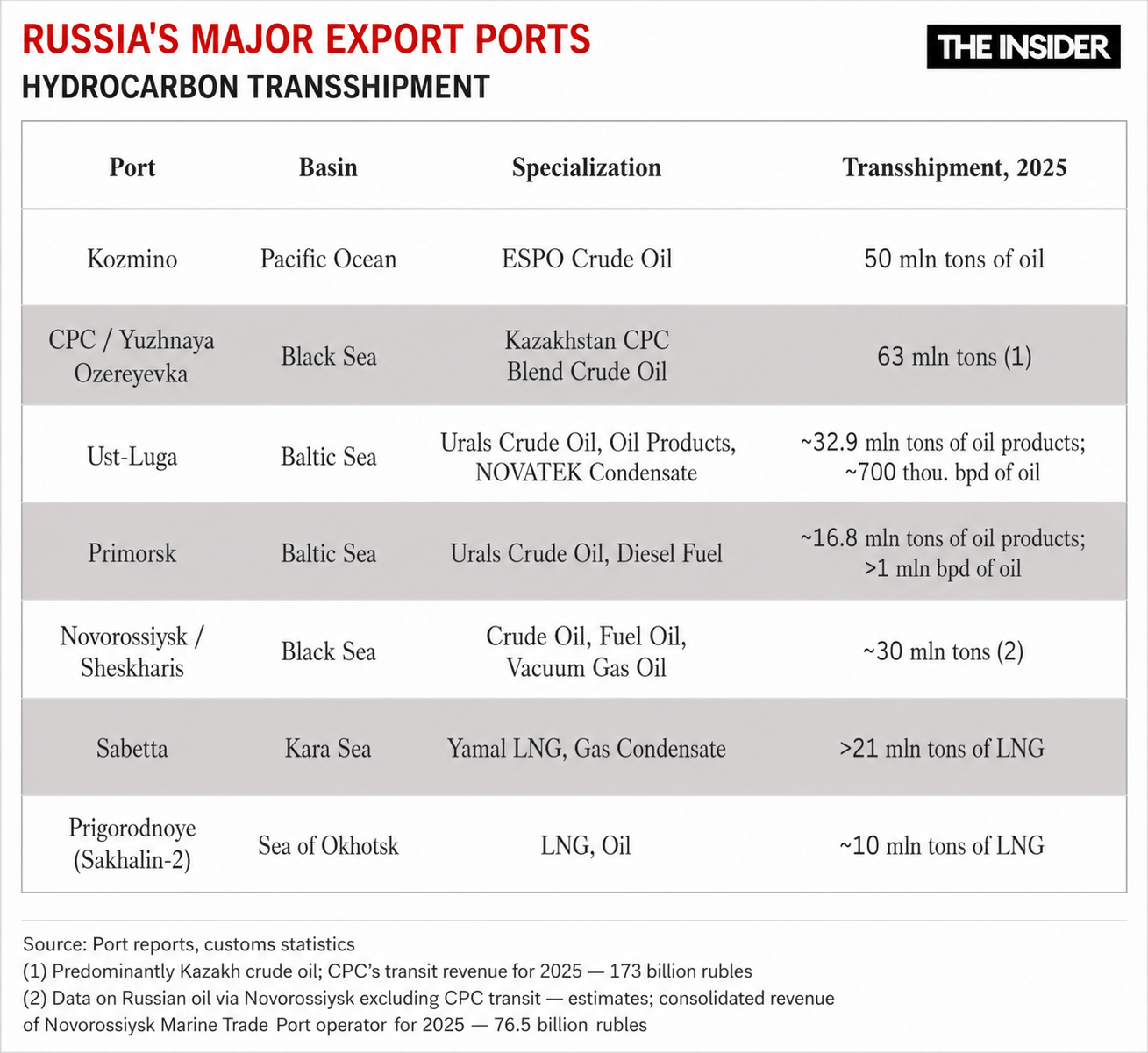

Russia's oil and gas export ports

Since the imposition of sanctions in 2022, Russia's seaborne export infrastructure has become the nerve center of the country's oil economy, allowing exports to reach China, India, and Turkey in order to offset the effects of the lost European pipeline market. In 2025, Russian ports handled 274.9 million metric tons of crude oil (+2.8% year-on-year) and 37.2 million metric tons of liquefied gas (including LNG). Maritime logistics has not merely survived — it is now carrying a heavier burden than ever before. That is why strikes on export ports are assuming increasing strategic importance.

Maritime logistics has not merely survived — it is now carrying a heavier burden than ever before

The Baltic route now handles exports of Urals crude to India and China. The key facilities are Ust-Luga, which ships crude oil and petroleum products (including Novatek’s stable gas condensate) at a rate of about 700,000 barrels per day. The port first came under attack in January 2025, when a strike on the Andreapol pumping station effectively shut down its operations, and it was targeted again in March and May of 2026. Russia's largest oil export terminal on the Baltic is the Port of Primorsk — the terminus of the Baltic Pipeline System, through which more than 1 million barrels of crude are exported per day. It was attacked on May 3, immediately halting shipments.

The Black Sea route consists of two major hubs. The Port of Novorossiysk (about 700,000 barrels per day) was damaged on May 23 by direct strikes on storage tanks and berth facilities operated by Chernomortransneft. The port operator reported revenue of 76.5 billion rubles ($979 million) for 2025, but given ongoing operational disruptions, that figure is expected to decline. Additionally, the nearby CPC Marine Terminal at Yuzhnaya Ozereyevka, which handles 75 million metric tons of Kazakh oil annually, was attacked in February 2025. Any disruption to its operations affects not only Russia but also Kazakhstan, creating diplomatic complications for any targeted restrictions.

The Pacific route serves as Russia's strategic reserve. The Port of Kozmino handles 46–50 million metric tons of low-sulfur ESPO crude annually, virtually all of it destined for China. For now, it remains beyond the range of Ukrainian drones.

The revenues of individual export terminals are not publicly disclosed, with the exceptions of financial results from the Novorossiysk Commercial Sea Port and the transit revenue of the Caspian Pipeline Consortium (CPC), which amounted to approximately 173 billion rubles ($2.25 billion) in 2025. For the remaining terminals, the best proxy is the consolidated financial performance of Transneft, whose IFRS revenue reached 1.44 trillion rubles ($18.72 billion) in 2025. The company transports about 12 million metric tons of Kazakh oil annually, while the remainder is Russian crude, much of it destined for export. Transneft's stable revenue can therefore be viewed as an indirect indicator of the resilience of Russia's export shipments.

Pipelines are burning, too

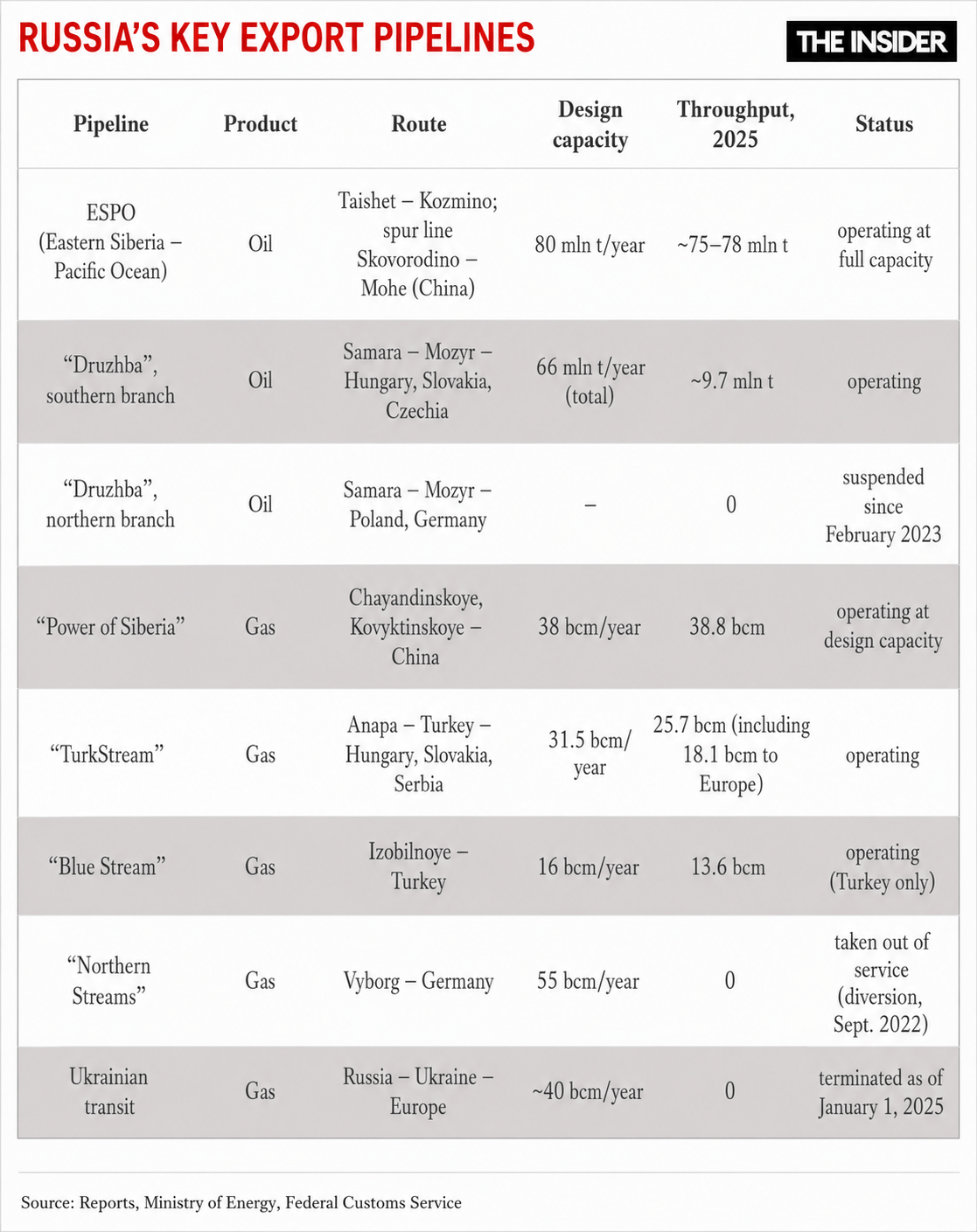

Russia's pipeline network has followed two very different trajectories since February 2022: one for oil and another for natural gas.

On the one hand, the oil pipeline system operated by Transneft (78.6% state-owned) transports more than 80% of all oil produced in Russia. In 2025, total throughput reached 447 million metric tons, including 435 million metric tons of Russian crude and 12 million metric tons of Kazakh oil, though these figures also include domestic deliveries. The group's revenue totaled 1.44 trillion rubles ($18.72 billion), a year-on-year rise of 1.2%, while net profit fell to 226 billion rubles ($2.94 billion) — down by 19.6%, partly because the corporate profit tax rate was raised to 40%.

The Eastern Siberia-Pacific Ocean (ESPO) pipeline carries about 80 million metric tons of crude annually. Of that, 30 million metric tons are delivered directly to China via the Amur River crossing, while just under 50 million metric tons are shipped through the Port of Kozmino (also to China, as noted above). The ESPO pipeline is operating at full capacity and remains the only major export oil pipeline whose infrastructure has not come under attack. As for the Druzhba pipeline, its southern branch to Hungary and Slovakia remains in operation, transporting about 9.7 million metric tons in 2025, while the northern branch serving Poland and Germany has been shut down since February 2023.

Since 2022, the natural gas pipeline sector has undergone its biggest structural upheaval in half a century. Ukrainian transit — historically the main route for Russian gas exports to Europe — ceased on January 1, 2025. The Nord Stream pipelines have been out of service since they were sabotaged in September 2022, meaning the only remaining operational route to Europe is TurkStream, with a capacity of 31.5 billion cubic meters per year. In 2025, about 18 billion cubic meters were delivered to European customers through the pipeline.

At the same time, the Power of Siberia pipeline reached its designed capacity, allowing Gazprom to supply more natural gas to China than to the entire European Union for the first time last year – 38.8 billion cubic meters. The compensation, however, is far from equivalent. Prices for gas sold to China are linked to a basket of petroleum products and are subject to a substantial discount, while the lack of alternative export routes leaves Moscow with little bargaining power.

The lack of alternative export routes leaves Moscow with little bargaining power in selling oil to China

The damage caused by strikes on oil pumping stations (OPSs) is concentrated not in the facilities themselves but in the disruption of the export flows that follows, making these stations targets with a disproportionately large economic impact. For example, the Yaroslavl-3 oil pumping station, which serves the Surgut-Polotsk pipeline, was struck twice in May, with both attacks sparking fires in storage tanks. The attacks threatened crude oil deliveries to two of Russia's largest Baltic export ports.

What has changed since 2022

Over the past four years, the war has fundamentally reshaped Russia's oil and gas economy. The industry has survived, but it now operates under dramatically different conditions: lower revenues, a major shift in export markets, higher costs, and mounting pressure on infrastructure.

Oil and gas condensate production has declined relatively modestly, from 524 million metric tons in 2021 to 516 million metric tons in 2024. That decrease is primarily the result of OPEC+ production quotas rather than sanctions alone. The natural gas sector has suffered much more severely due to the combined effect of three factors. The sabotage of the Nord Stream pipelines in September 2022 eliminated export capacity of 55 billion cubic meters per year, and the end of Ukrainian transit in January 2025 cut off another roughly 40 billion cubic meters. Meanwhile, European demand for Russian gas has collapsed as the continent diversified its supplies — from more than 150 billion cubic meters annually before the war to about 18 billion cubic meters in 2025. The EU's full embargo on Russian gas, including LNG, is set to take effect in 2027 and will be phased in gradually.

In short, gas exports to Europe have fallen to their lowest level since 1973, and while the Power of Siberia pipeline has partially offset the lost volumes, it cannot come anywhere close to recouping lost revenues. As for oil exports, shipments to Europe have plunged from 175 million metric tons in 2022 to fewer than 25 million metric tons in 2025.

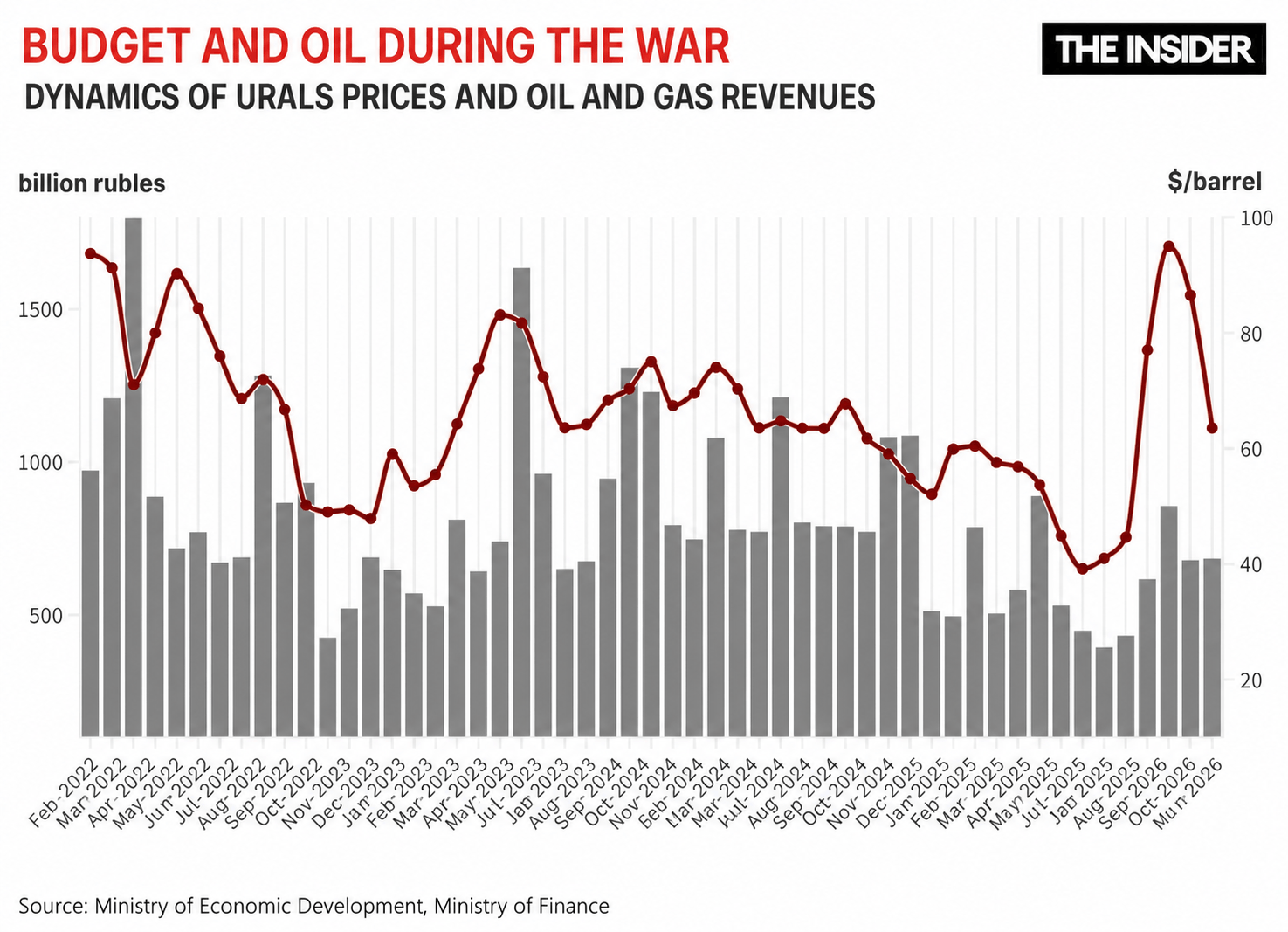

China and India have replaced Europe as Russia's main customers, now accounting for about 80% of the country's total oil exports. This pivot to Asia has come at the cost of severe price discounts. The discount of Urals crude to Brent, which had previously averaged $12–13 per barrel, reached $23.5 in November 2025, while in December the price of Urals delivered to Novorossiysk fell to $34.5 per barrel — approaching the lower bound of profitability for production at mature oil fields.

The Iran crisis significantly altered the picture, but perhaps only temporarily. At the height of the escalation in April 2026, spot prices for Urals exceeded $114 per barrel, while the monthly average, according to the Ministry of Economic Development, reached $94.87, narrowing the discount to Brent to its lowest level since the end of the previous year. However, this market environment has proved highly unstable, as demonstrated by the decline in oil prices since June.

As tensions in the Middle East ease and OPEC+ members increase production — along with the UAE, which withdrew from OPEC and OPEC+ on May 1 — the price premium is likely to erode, leaving Russia dependent on discounted Asian markets yet again. Moreover, the rise in Urals prices has already affected the fuel price damping mechanism. After making only minimal compensation payments at the beginning of the year — when oil prices were high — the federal budget was forced to sharply increase damping payments to oil companies, reaching 204.3 billion rubles ($2.66 billion) in May.

New and old vulnerabilities

The main vulnerability of Russia's oil industry — as exposed in 2026 — is the systemic concentration of refining capacity within strike range of Ukrainian drones. FP-1 ("Liutyi") long-range UAVs can reliably hit targets at distances of 1,500-2,000 kilometers, putting every refinery west of the Ural Mountains within reach. And the strike on the Omsk Oil Refinery demonstrated that even facilities east of the Urals are no longer safe. The shift in targeting toward secondary processing units — cracking, reforming, and hydrocracking facilities — marks a qualitative change in the Ukrainian campaign.

Because these units are custom-built, rely on imported equipment now blocked by sanctions, and take months to repair, it is impossible to replace lost capacity with domestic production in the short term. Mandatory anti-drone defenses at refineries do not solve the problem. Russia simply lacks sufficient electronic warfare systems and Pantsir air defense systems to protect ten or more refineries spread across a zone extending up to 1,500 kilometers from the front, especially given the scale and coordination of the attacks.

Lost refining capacity cannot be restored quickly using domestically produced equipment, and anti-drone defenses at refineries are not enough to solve the problem

At the same time, pressure on Russia's shadow fleet is intensifying. Whereas tanker detentions were once isolated incidents, EU countries arrested or confiscated at least seven tankers in the first quarter of 2026 – almost as many as during all of 2025. An even more significant precedent for Russia came in January 2026, when the United States seized the tanker Marinera (formerly Bella 1) in the Atlantic. While the vessel was being pursued off the coast of Venezuela, it switched to the Russian flag in an apparent attempt to avoid interception. The episode demonstrated that the U.S. Coast Guard and Navy are prepared to detain vessels sailing under the Russian flag even in international waters.

The strategic vulnerability in the gas sector is Novatek’s Yamal LNG project at Sabetta. The project has so far avoided sanctions, but more than 70% of its exports still go to the EU — around 15 million metric tons worth €7.2 billion in 2025. However, the EU has already agreed to phase out all imports of Russian gas, including LNG, by the fourth quarter of 2027. Even before the formal embargo takes effect, the ban on LNG transshipment through the ports of Zeebrugge and Montoir has complicated logistics for Arc7 ice-class LNG carriers.

A global recession, however, remains the most dangerous scenario. By some estimates, every $10 decline in the price of Brent below the budget benchmark of $59 per barrel would cost the federal budget 1.5–1.8 trillion rubles ($19.5–23.4 billion) annually. The discount on Urals crude relative to Brent, combined with a strong ruble, would only amplify the effect by reducing ruble-denominated Mineral Extraction Tax (MET) revenues.

Meanwhile, the complete or partial withdrawal of Western oilfield service companies from the Russian market has increased operating costs. Wells at mature fields, where water cut exceeds 80–90%, require continuous hydraulic fracturing to sustain production. Of course, the technology and equipment needed for these operations have been restricted by sanctions.

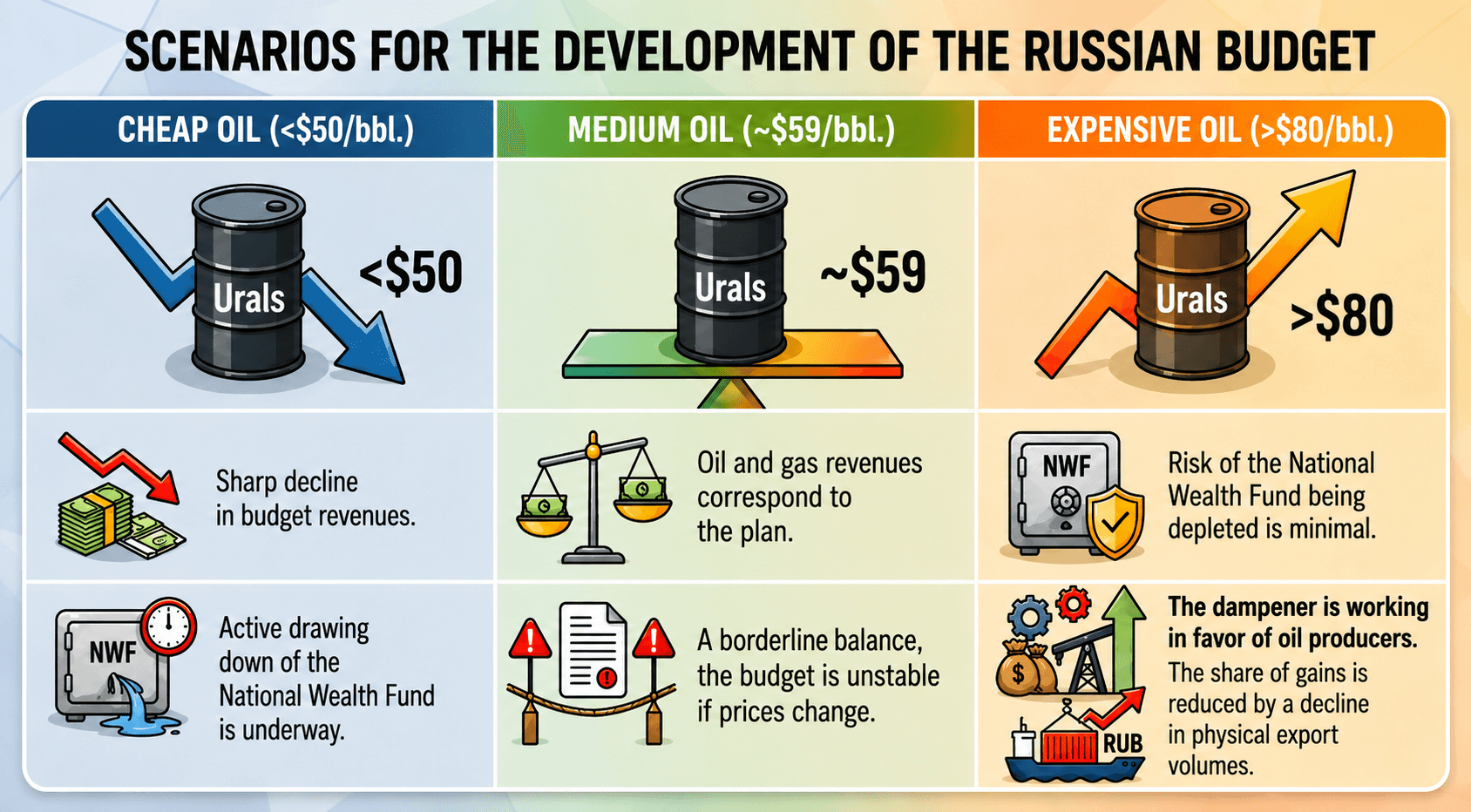

Three paths for Russia's budget

Scenario one: fiscal collapse within a year. If oil prices remain low — as they did between November 2025 and February 2026, when Urals traded below $50 per barrel — oil and gas revenues would decline sharply. According to the Ministry of Economic Development, when Urals trades at $40–45 per barrel, monthly oil-and-gas revenues amount to only about 400 billion rubles ($5.2 billion), roughly one-third of the planned level. If Urals falls to $35 per barrel and remains there for several months, annual oil-and-gas revenues could even fall to below 5 trillion rubles ($65 billion), compared with the budget target of 8.92 trillion rubles ($116 billion).

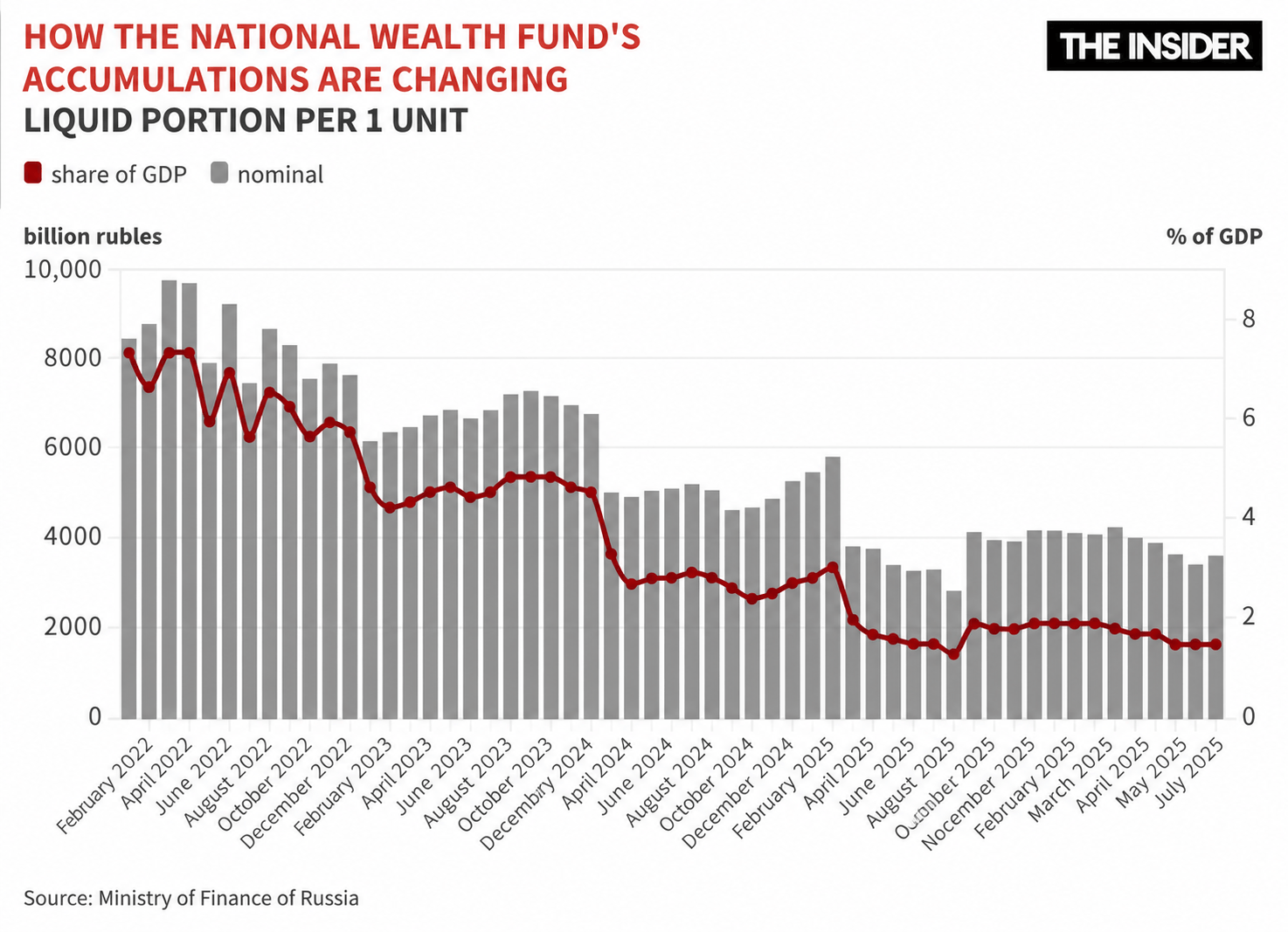

This scenario becomes significantly worse if Ukrainian strikes on oil refineries continue. Damage to these facilities reduces not only refining capacity but also oil production itself, meaning that revenues from the Mineral Extraction Tax (MET) and the Additional Income Tax (AIT) decline regardless of oil prices. The National Wealth Fund (NWF) must then shoulder additional pressure by compensating for the lost budget revenues. As of July 1, the fund's liquid assets stood at just 3.6 trillion rubles ($46.8 billion). If they are spent at a rate of 200–300 billion rubles ($2.6–3.9 billion) per month, those reserves would last for roughly one to one and a half years — and even less under a crisis scenario.

Scenario two: a fragile equilibrium. If oil prices remain around the budget benchmark, with Urals trading at approximately $59 per barrel, oil-and-gas revenues would broadly match the planned 8.92 trillion rubles ($116 billion), while fuel damping payments would remain moderate and predictable. Under this scenario, the budget avoids acute pressure but also generates no windfall revenues. The entire fiscal framework balances on a knife's edge: with the exchange rate unchanged, every $10-per-barrel move in oil prices away from the benchmark adds or subtracts roughly 120 billion rubles ($1.56 billion) in monthly revenue, or about 1.4 trillion rubles ($18.2 billion) per year.

In practice, this means the "middle" scenario is an inherently unstable equilibrium that depends on factors beyond Moscow's control, including geopolitical developments, OPEC+ decisions, and changes in the Urals discount. Paradoxically, however, it is more favorable for Russia than either of the two extremes — very high or very low oil prices — because it allows the budget to be adequately funded without causing fuel damping payments to spiral upward.

The "middle" scenario is, in reality, a highly unstable equilibrium that depends on factors beyond Moscow's control

Scenario three: losing Asian markets. When oil prices are high — as they were in April-May 2026 when the average monthly price of Urals was above $80 per barrel — the federal budget should, in theory, receive a windfall. In practice, however, April demonstrated how this scenario actually works. With Urals averaging $94.87 per barrel (according to the Ministry of Finance), oil-and-gas revenues totaled only about 856 billion rubles ($11.13 billion) instead of the theoretical 1.3–1.4 trillion rubles ($16.9–18.2 billion). A strong ruble (averaging 77 rubles to the dollar instead of the 92 assumed in the budget) and fuel damping payments that absorbed 377 billion rubles ($4.90 billion) wiped out most of the potential gain.

In other words, the higher the oil price and the smaller the discount, the less competitive Russian crude becomes in Asian markets, which have grown accustomed to buying it at a discount relative to Middle Eastern or U.S. crude that carries no sanctions-related risks.

In other words, India and China are eager buyers of Urals primarily when it is cheap. As the discount narrows, part of that demand shifts to competing suppliers. Chinese and Indian refineries buy Urals not because they specifically need this grade of crude, but because the discount offsets higher transportation costs, sanctions-related risks, and its lower quality (Urals, for example, is heavier and contains more sulfur than Arab Light or Dubai Light). When the discount is $20-25 per barrel, as it was in late 2025, the economics are compelling. When it shrinks to $5-8 per barrel, as it did in April 2026, the price difference is no longer sufficient to compensate buyers for sanctions-related risks, higher insurance costs, and longer shipping routes.

At that point, some buyers begin switching to Middle Eastern crude grades — not because Urals has become expensive in absolute terms, but because the price incentive to tolerate its unique risks and additional costs has disappeared.

In June, the "middle" scenario prevailed, emerging after tensions eased between the United States and Iran. By early July, Brent crude was trading at around $70 per barrel, while the average price of Urals used by Russia's Ministry of Finance to calculate the Mineral Extraction Tax (MET) had fallen to $63.52 per barrel, down from $86.52 in May.

According to Citigroup estimates, Brent crude could decline to $60 per barrel by the end of the year if shipping through the Strait of Hormuz returns to normal. In that event, the first scenario — low oil prices and the rapid depletion of Russia's financial reserves — would see the federal budget deficit rise even further.

Regardless of which price scenario ultimately prevails, policymakers must now contend with an entirely new factor: government payments to subsidize fuel imports under a new mechanism. It is one of the measures the Russian government has introduced to address the country's worsening fuel crisis. When oil prices are high — a state that would ordinarily benefit the federal budget — the Russian government is obligated to pay hundreds of billions of rubles to domestic oil companies while also providing compensation to fuel importers.