As discussions about the misappropriation of funds from Probusinessbank resurface, The Insider offers an analysis of the key events, drawing on numerous previously unpublished interviews with Zheleznyak and Leontiev conducted by the author four years ago. A review of the documents they provided, along with their own accounts, reveals that the infrastructure established by Zheleznyak and Leontiev was actively used to launder hundreds of millions of dollars, evade legal regulations, and move funds offshore — where a large portion disappeared before the Deposit Insurance Agency (ASV) could intervene.

- 1.Introduction: The Probusinessbank ecosystem

- 2.Chapter 1: Where did the money come from? Prosecutors' undeclared cash

- 3.Chapter 2. External aspects: Non-bank business of Probusinessbank

- 4.Chapter 3. Disappearing millions: repo deals and off-balance sheet infrastructure

- 5.Chapter 4: Alice in Wonderworks: Profits for owners, risks for shareholders

- 6.Where the money went

Introduction: The Probusinessbank ecosystem

In 2020, the author of this article spent many hours in discussions with the founders of the Life financial group, Sergey Leontiev and Alexander Zheleznyak, and received a large set of documents from them, many of which had not been published at the time. The founders of Life, which included Probusinessbank and several other banks, openly acknowledged that their business did not operate as a bank in the usual sense. In reality, Probusinessbank was an informal network of interconnected companies involved in various businesses, including real estate, factoring, pawnshops, and debt collection agencies.

Current regulations restrict banks from simultaneously being both the owner and the lender of their own businesses, so the bank conducted its operations with its companies through a series of intermediaries, with some of these activities carried out via offshore entities. A significant portion of the funds the bank attracted for its investments consisted of undeclared cash from their friends and relatives (indicating corrupt origins), and also from Russian prosecutors. Probusinessbank transferred this money to offshore companies, and some of the money returned to the bank as subordinated loans — thereby converting liquidity into capital to improve its financial reporting. The rest of the money was used for high-risk operations.

After multiple violations were uncovered, Probusinessbank’s license was revoked. It was revealed that the bank’s most liquid assets were pledged to brokers who had taken out loans backed by these assets — and that the assets had disappeared by the time the license was revoked. When the Deposit Insurance Agency (ASV) took control, the bank was missing several hundred million dollars.

It was also revealed that Probusinessbank funds were used by the owners as unsecured loans for their own risky “blue chip” stock trading, allowing them to shift the risks onto shareholders and depositors.

Let’s break down the key elements of this inventive scheme.

Chapter 1: Where did the money come from? Prosecutors' undeclared cash

One of Probusinessbank's primary methods of attracting investments was selling promissory notes issued by its affiliated companies. According to Zheleznyak, these notes were guaranteed by the bank itself. The promissory notes offered very high returns — up to 12% annually in foreign currency, significantly above market rates for the 2010s in Moscow. In testimony given by Leontiev in a U.S. court, he explained the economic rationale behind the high interest rates by stating that every million dollars raised this way as bank capital enabled them to issue up to $10 million in “ordinary” loans.

According to Zheleznyak, over $300 million was raised through these promissory notes. Probusinessbank did not go to great lengths to hide that these funds largely consisted of undeclared cash from prosecutors.

Zheleznyak explained that the main buyers of the promissory notes were the beneficiaries of the Avilon car dealership company: Alexander Varshavsky and Kamo Avagumyan. (Avagumyan was formerly the representative of the Armenian General Prosecutor's Office in Russia, and one of Avagumyan's sons worked in the Russian General Prosecutor's Office). Promissory notes were also issued to Avagumyan's relatives, including Diana, the daughter of the late Russian Deputy Prosecutor General Saak Karapetyan, as well as other people close to Avagumyan and Varshavsky. Zheleznyak indicated that a portion of the funds contributed by Avagumyan and his circle actually belonged to other individuals. According to the beneficiaries of Probusinessbank, these funds likely originated from the Russian General Prosecutor’s Office.

The beneficiaries were all served by the bank's VIP department, which was almost entirely focused on this group of clients — and was located in the same building as Avilon’s headquarters. The head of the VIP department, “NN,” mentioned in a conversation that she often felt uncertain whether she worked for Avilon or Probusinessbank, as 80% of her time was dedicated to serving Avilon clients. Several full-time cashiers were assigned specifically to handle cash deposits from Avagumyan’s associates.

In a discussion with the author, former Probusinessbank shareholder Sergey Leontiev initially maintained that the bank strictly verified the origin of cash deposits. However, when confronted with NN's story in which she stated that no one ever questioned the source of the funds, Leontiev did not dispute it, admitting that he “only learned about this later.”

NN explained, and Zheleznyak confirmed, that the relationship with the Avagumyan and Varshavsky families became very close, almost “family-like” — and mutually beneficial. The bank and its owners bought cars from Avilon, while Avilon used the bank for short-term loans and managed employee accounts. The beneficiaries of Avilon and other associates of Avagumyan handled the personal finances of their families and household staff through Probusinessbank — even their Filipino housekeepers received services. The bank maintained entire “clusters” of affairs for each family, handling their various needs. For instance, the bank purchased a Bentley for VIP client Igor Renich in his absence and delivered it to his country home. They truly maintained “family-style” relationships — inviting each other to corporate events, celebrating birthdays, and engaging in similar social activities.

According to NN, over time, Avagumyan’s associates began to exert pressure on the bank’s employees, “twisting their arms.” For example, Boris Zuev once demanded that a promissory note be issued in the name of “B. Zuev,” without including his full name or patronymic, which was illegal. Nevertheless, the bank complied because it did not want to upset such a valuable group of clients. When NN issued a promissory note for Diana Karapetyan, the daughter of the Russian Deputy Prosecutor General, she initially hesitated because Diana was not present, and only a passport scan was provided. However, the management ultimately ordered her to proceed.

The VIP department manager did not want to issue a promissory note for Diana Karapetyan, the daughter of the Russian Deputy Prosecutor General, because Diana herself was not present. Only a scan of her passport was provided, but the management ordered the VIP department to proceed

No one asked any questions about the origin of the hundreds of millions of dollars in cash that NN or her employees counted. Kamo Avagumyan would tell her, “The less you know, the better you sleep.” He could come in and say, “You know whose money this is,” implying that Zheleznyak already had the promissory note recipient's details. She would simply take the box, count the cash, and issue the promissory note.

According to Zheleznyak, Kamo Avagumyan came to Moscow through his connections with the Armenian General Prosecutor's Office. This was the source of his close ties with Russian prosecutors. Avagumyan is described as a man with a generous Caucasian spirit, known for his loyalty — i.e., someone who would not abandon his friends when they are in trouble. One of his sons, Georgy, worked in the Russian Prosecutor General's Office. Kamo became close with many influential figures, including the legendary sons of Prosecutor General Yuri Chaika, then-head of the FSB Banking Department Viktor Voronin, and future Moscow region governor Andrey Vorobyov. All of these people were involved in high-profile corruption scandals at one time or another.

The “friends” of Probusinessbank, who allegedly carried “suitcases full of cash” into its office (as mentioned in one of the court rulings), introduced its owners to several law enforcement officials, whom the bank later tried to use to its advantage. For example, according to Zheleznyak’s sworn testimony in U.S. courts, in 2014 Avagumyan and Varshavsky offered Zheleznyak and Leontiev a deal. Zheleznyak claims that Avagumyan warned them that the state was planning to revoke the license of Bank24, which was part of the Life financial group, and Avagumyan and Varshavsky offered to prevent this from happening on the condition that half of Life’s shares would be transferred to Avilon for free. Zheleznyak asserts that the seriousness of this threat was based on Avagumyan’s long-standing business ties with Chaika’s sons. Avagumyan allegedly implied that the dividends from half of Life would be split between the Prosecutor General's Office and Avilon. The “final decision” regarding Bank24 supposedly rested with Prosecutor General Chaika and the head of the FSB’s Department K, Viktor Voronin.

Zheleznyak claims that the proposal to take over Bank24 was discussed with Anatoly Palamarchuk at the Prosecutor General's Office. Palamarchuk convinced Zheleznyak that the Central Bank's investigation into Bank24 was very serious but suggested “talking” to Yuri Chikhanchin, the head of Rosfinmonitoring, and Mikhail Sukhov, the deputy chairman of the Central Bank of Russia. According to Zheleznyak, at the next meeting, Avagumyan confirmed that all the details of the upcoming division of Life CJSC had been worked out under Voronin's leadership. However, an additional condition arose: at this stage, Zheleznyak and Leontiev were required to hire a former FSB officer as vice president of Life, with a generous salary for his “supervision.” Zheleznyak and Leontiev agreed to this demand and sent a corresponding letter to the FSB. Afterward, Zheleznyak claims, a meeting with Kirill Cherkalin took place, during which Cherkalin confirmed that the letter had been processed. Avagumyan, according to Zheleznyak, also organized a meeting for him and Leontiev with Elvira Nabiullina, the head of the Central Bank of Russia.

Despite these efforts, in September 2014, Bank24’s license was revoked, and its assets were transferred to Otkritie Bank. In 2019, Cherkalin was arrested, and 12 billion rubles in cash were found during a search of his apartment.

The fact that Probusinessbank was effectively laundering money for Russian prosecutors was confirmed during court proceedings in various jurisdictions. Alexander Zheleznyak claims that by the time Probusinessbank’s license was revoked, about $80 million in investments belonged to Avagumyan’s and Varshavsky’s friends and relatives. A significant portion of Avagumyan’s and Varshavsky’s personal investments had already been spent on real estate, a yacht, and airplanes. Officially, Avagumyan still held promissory notes worth about $30 million in his own name and a similar amount in Avilon’s name (as stated by Zheleznyak and confirmed by U.S. court documents). According to Zheleznyak, this $30 million actually belonged to Palamarchuk, the Chaika family, the Karapetyans, and the Voronins. It was this $30 million that was the subject of discussions in the New York courts.

Zheleznyak claims that by the time Probusinessbank’s license was revoked, around $80 million in investments belonged to Avagumyan’s and Varshavsky’s friends and relatives

The fact that Avagumyan and Varshavsky were not the ultimate beneficiaries of the “frozen” investments registered in their names was also confirmed by Varshavsky himself. During a confidential meeting with Zheleznyak and Leontiev in London — a meeting that was recorded and later documented in U.S. court materials — Varshavsky said that if he flew to Moscow without a written commitment from Leontiev to pay the debts of companies affiliated with the bank from the banker’s personal funds, Varshavsky would “lose his head.”

Chapter 2. External aspects: Non-bank business of Probusinessbank

Zheleznyak explained the circulation of cash based on the bank’s investment goals. According to him, it was very difficult for the bank to conduct business in the real sector. Among the types of business Probusinessbank wanted to engage in, Zheleznyak mentions real estate development, factoring, and pawnshops:

“Well, it's business, you know what I mean? The bank doesn’t run a business. There's a lot of regulation, because it’s real business. A gold pawnshop. How can a bank run 'Zolotoi Lombard' (lit. “Gold Pawnshop”)? And if the bank acts as the founder of a gold pawnshop, it can’t lend it money due to regulatory restrictions. That’s why business projects were created, where the bank acted as a creditor, earning both interest and profit from the project.”

In other words, Probusinessbank's senior management did not hide the fact that it de facto controlled businesses related to the bank while simultaneously lending to them and making profits, fully aware that this was against the law.

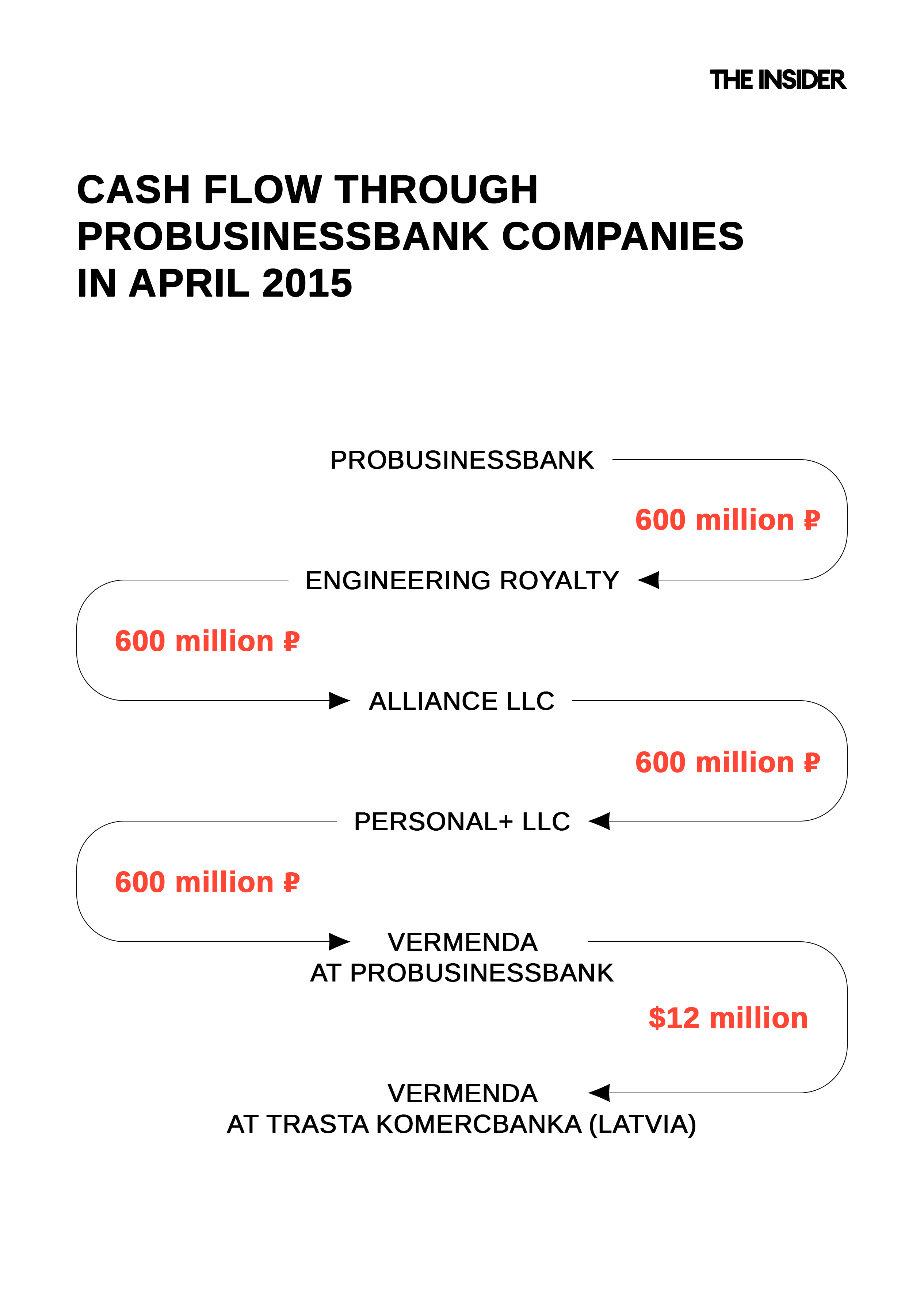

According to Alexander Zheleznyak, the financial group Life operated like an “entrepreneurial bank,” with around 300 divisions functioning as independent businesses, each with separate profit and loss accounts. Of the 15,000 bank employees, approximately 5,000 worked as “partners,” meaning they received a share of the profits. These divisions included both separate legal entities (about 30%) and internal departments (about 70%). Some business divisions could accumulate excess cash (for example, a department dealing with individual depositors), while others might require cash (for instance, to purchase lucrative financial instruments abroad or to issue loans). This is where the “entrepreneurial bank” stepped in, helping to transfer funds from one division to another through a network of companies connected by hubs. According to Zheleznyak, one of the main hubs was a company called Vermenda.

The former owners of the bank acknowledge that investment in these businesses included the “undeclared cash” mentioned above. Thus, Probusinessbank received suitcases of cash from employees of the Prosecutor's Office and funneled these “dirty” funds not only through the bank itself, but also through its businesses — turning them into what looked like fully legitimate income.

Probusinessbank received suitcases of cash from employees of the Prosecutor's Office and funneled these “dirty” funds not only through the bank itself, but also through its businesses, turning them into what looked like fully legitimate income

In the process of financing its projects, Probusinessbank regularly transferred large sums of money through a chain of companies that did not engage in any real-world economic activity.

Zheleznyak and Leontiev explained that this chain of intermediaries (or “operational firms,” as Zheleznyak referred to them) was needed in order to avoid the regulator's scrutiny, as lending to affiliated companies was prohibited. According to them, one intermediary might not be enough, as the Central Bank could start tracking the next “level of investment” at some point during a transaction. A chain of three intermediary firms allowed them to effectively transfer credit funds between affiliated legal entities while formally appearing to comply with regulatory standards.

It is worth noting that this chain of intermediaries not only helped the bank avoid questions from the regulator but also served as the perfect infrastructure for turning hundreds of millions of “gray” cash from Russian prosecutors into “clean money.”

Intermediaries and a network of hundreds of legal entities were not the only innovations of the Life group. Offshore companies, where the majority of funds were funneled, also played an important role in this ecosystem.

Chapter 3. Disappearing millions: repo deals and off-balance sheet infrastructure

Zheleznyak and Leontiev admit that they purposefully funneled bank funds into a number of offshore companies, which can be referred to as off-balance sheet entities, or the bank's “external tier.” Since it was impossible to do this directly (lending to an entity with no assets would have ruined Probusinessbank's financial statements), it was arranged through a transaction formally structured as a repo deal with reputable brokerage firms (Otkritie, BCS, Dinosaur Securities), which provided loans to the external tier entities (Ambika, Merianol, Vermenda) backed by highly liquid Probusinessbank assets — namely U.S. Treasury bonds and other securities. Formally, the bonds remained on the bank's account at the brokerage firm, but they were also simultaneously — de facto — serving as collateral for the offshore entities' financial activities.

Once the funds got into the “external tier,” Zheleznyak and Leontiev could manage them as they pleased, without any oversight from the regulator.

What was the purpose of this cash infusion? Zheleznyak explains that these offshore entities issued subordinate loans back to Probusinessbank, meaning the bank essentially invisibly converted liquid assets (e.g. Treasury bonds) into capital, which looked good for reporting purposes.

Setting aside the question of whether deceiving the regulator is justifiable, it should be noted that only $90 million in subordinate loans was returned, which is several hundred million dollars less than was withdrawn.

Thus, like the intermediary firms and the network of numerous legal entities, the offshore “external tier” served as a tool to shift part of the money from a relatively transparent and regulated financial system into a “hands-on management” system, where it ultimately disappeared.

The offshore “external tier” served as a tool to shift part of the money from a relatively transparent and regulated financial system into a “hands-on management” system, where it ultimately disappeared

One of the striking examples of this “hands-on management” regime is the story of the Wonderworks Investments fund.

Chapter 4: Alice in Wonderworks: Profits for owners, risks for shareholders

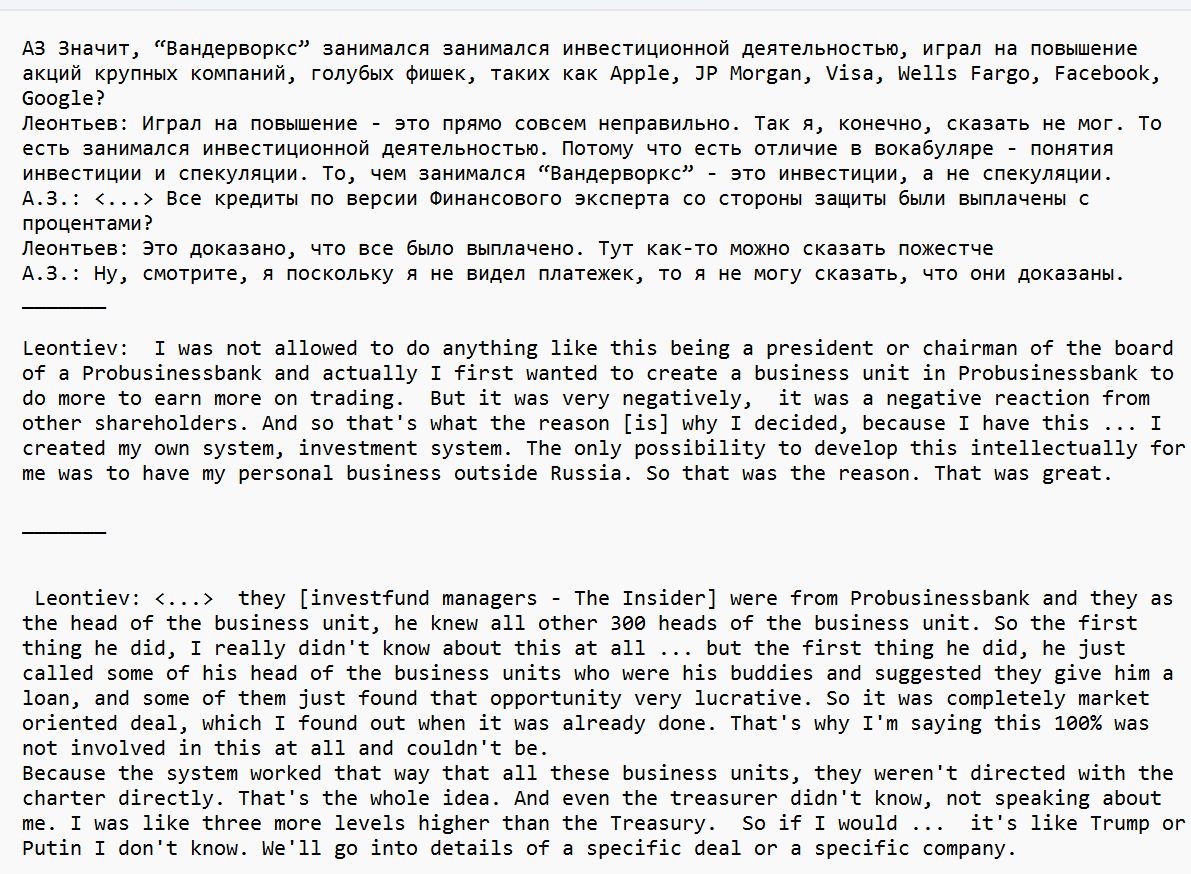

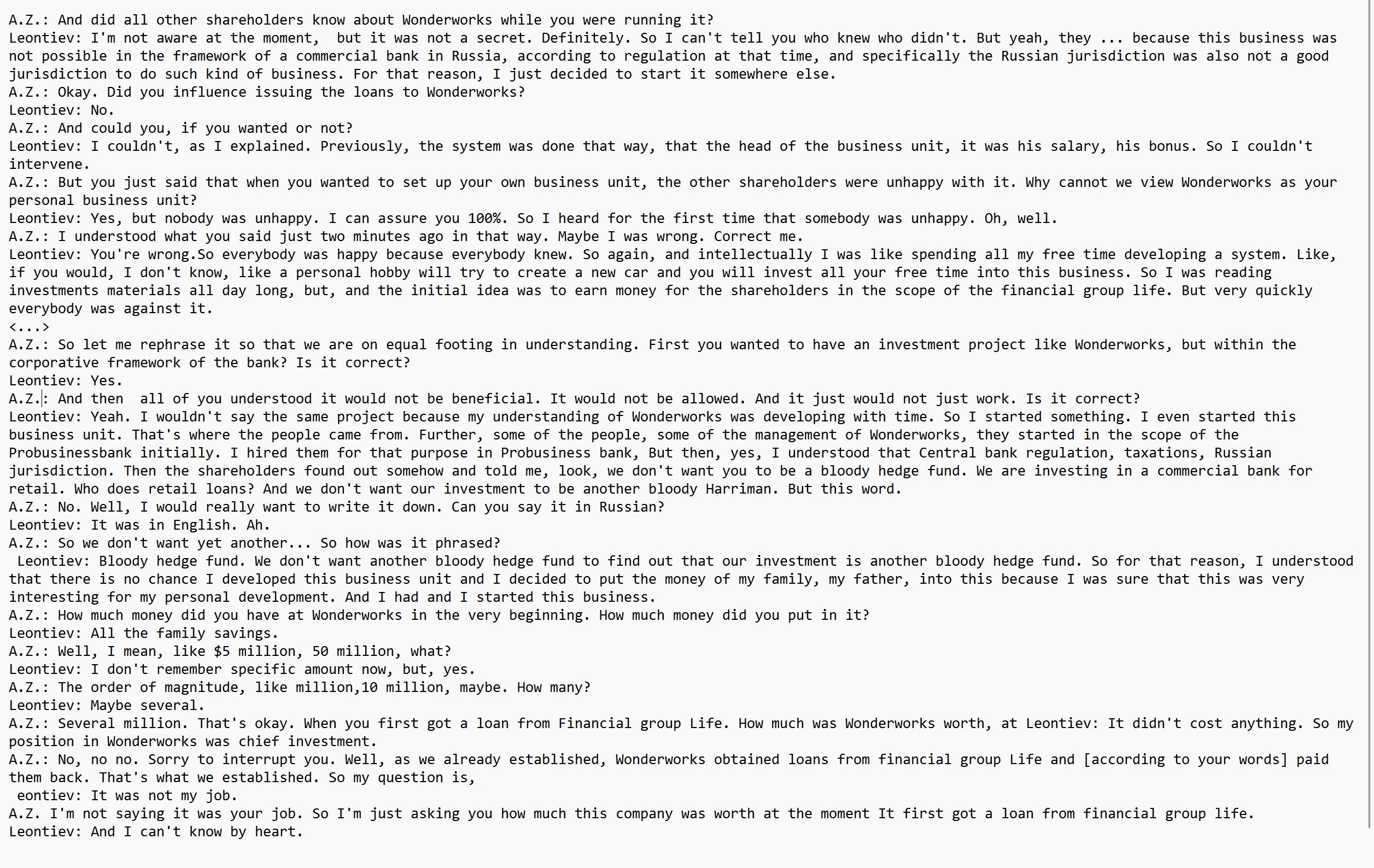

Wonderworks Investments (also known as Wonderworks Assets) belonged to Sergey Leontiev's family trust and received a staggering $360 million in loans at an interest rate of 3-5% from offshore entities controlled by the owners of Probusinessbank (Sergey Leontiev insists on referring to them as “business units”): Finbay, Dunning, Vermenda, and Greenex. Wonderworks invested in shares of major companies — blue-chip stocks like Apple, JPMorgan, Visa, Wells Fargo, Facebook, and Whole Foods. The turnover for these operations exceeded $700 million.

Why wasn’t the trading conducted through the bank’s main legal entities? As in other instances, Probusinessbank’s leadership explained that this was done to evade the ever-watchful eye of the regulator. The Central Bank would have required significant reserves for risk insurance when purchasing blue-chip stocks. Additionally, other bank shareholders deemed such trading to be too risky.

Sergey Leontiev explained that he initially proposed the idea for Wonderworks through the bank's corporate structure, but it was rejected by other managers, who said, “We don’t want another bloody hedge fund.”

Therefore, according to Leontiev, the idea of making off-balance-sheet investments in blue-chip stocks was realized in a slightly modified form by using his personal start-up capital (several million dollars), along with loans from Probusinessbank. Employees for his personal trust were also borrowed from Probusinessbank.

The ease with which Probusinessbank issued loans to Wonderworks, according to Leontiev, was explained by the fact that Probusinessbank employees knew the employees of Wonderworks, having worked with them previously. Leontiev claimed that he could not influence the loan approval for his family business.

In simple terms, Leontiev played the stock market game (which he referred to as “investments”) using depositors' money through unsecured loans. The majority of the profits went into his own pocket, while the depositors carried the primary risks.

After taxes, Wonderworks' investments brought Leontiev more than $190 million, which he placed in the family trust Legion, registered in the Cook Islands.

Where the money went

Based on the available data, confirmed by documents provided in 2020 and the direct testimonies of Zheleznyak and Leontiev, the owners of Probusinessbank set up an infrastructure involving a network of intermediaries and a “second tier” of off-balance sheet entities. This setup effectively concealed risky operations from regulators and facilitated the “processing” of hundreds of millions of dollars in cash brought to the bank in suitcases by friends and relatives of personnel from the Prosecutor-General’s Office.

The documents and explanations from Zheleznyak and Leontiev also reveal that they funneled cash into off-balance sheet entities under the pretense of legitimate investments in safe securities, such as U.S. Treasury bonds. While a small portion of the siphoned funds returned as subordinated loans — necessary for creating the illusion of solid financial reporting — the vast majority of the funds, amounting to hundreds of millions of dollars, never returned to the bank and had disappeared by the time the ASV — the Deposit Insurance Agency — was able to evaluate the company’s books.

The money that ended up in Ambika and Merrianol could have left a trace if it had been invested in the bank’s “business units,” in which case Probusinessbank would have gained claim rights to these investments once the collateral under the guarantee had been seized. However, the ASV's inventory reveals no such claims.

Additionally, from the explanations of Zheleznyak and Leontiev, it is clear that Leontiev was trading on the stock market using unsecured credit for his personal investment fund, despite the management's objections, thus shifting the risks onto depositors and shareholders.

In a bankruptcy, the bank’s owners should be the last to receive funds (if they receive anything at all), much like a captain should be the last to leave a sinking ship. In this instance, however, it was the depositors who suffered first, while the money funneled into the offshore accounts proved impossible to be traced.

The subsequent carving up of Probusinessbank's assets by the ASV does not change the conclusions drawn above, which are based on earlier events and documents.